On the Securities Action of Thursday, January 29, 2015

“Omnia Possidere”

“Just Buy Everything!”

I’m still bullish and believe stock prices will go higher. Today was a great day for stocks on Wall Street; Stocks roared forward and fixed income rallied. Stocks traded downwards until approximately 10amCT, when they reversed course and rallied strongly, finishing up for the day. The DJIA fell to 17,136 before reversing to close at 17,417. The S&P500 fell to 1,989 before reversing and finishing at 2,021.

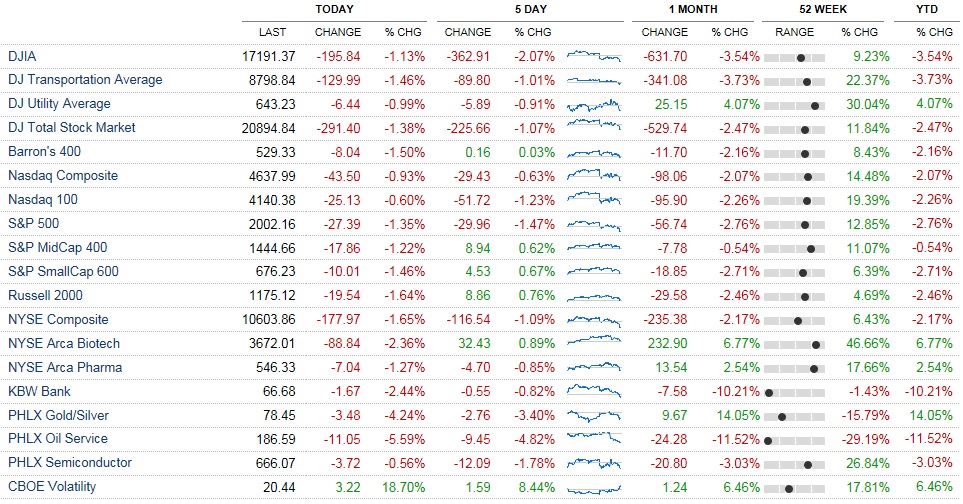

The DJIA closed up +225.48 or +1.31% to 17,416.85, the S&P500 was up 19.09 points or +0.95% to 2,021.25, the S&PMidCap400 was up +10.69 points or +0.74% to 1,455.35. Volatility (as measured by the VIX) imploded, and was down -1.68 points or -8.22% to close at 18.76.

The DJIA is now -3.79% off its trailing 12 month peak, the S&P500 is -3.45% of its 12 month peak, the S&PMidCap400 is -1.55% off its 12 month peak, the Nasdaq Composite is -2.73% off its 12 month peak, and the Russell 2000 is now -2.56% of its 12 month peak, the Wilshire 5000 is now -3.07% off its peak. XLF, an etf basket of financials, was +0.82% to 23.39, and is now -6.25% off its 12 month peak. I believe the markets (excluding the Nasdaq 100, and the Nasdaq Composite) are going to plow forward to new all time highs in the next week or two. The Nasdaq 100 and Nasdaq Composite have quite a bit of more territory to cover before striking new all time highs, set in March of 2000.

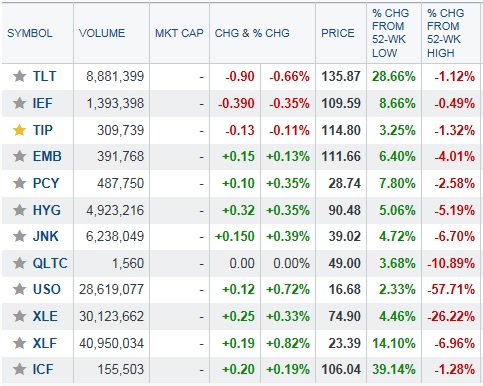

USO (oil) was up +0.72% to close at 16.68, XLE was up 0.33% to 74.90, RSX was down -1.27% to 14.81, CUBA was -2.46%% to 8.72. Oil seems to have stabilized here over the past few days. [http://finance.yahoo.com/futures]

In the Fixed income markets, Treasuries sold off, while the high yield sector rallied. TLT traded down -0.66% to 135.87, IEF was down -0.35% to 109.59, TIP was down -0.11% to 114.80, EMB was up +0.13% to 111.66, PCY was up +0.35% to 28.74, HYG was up +0.35% to 90.48, JNK was up +0.39% to 39.02, and QLTC was unchanged at 49.00. The 30 year Treasury yield settled at 2.33%, the 10 year Treasury yield settled at 1.77% [data from here: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield]. I continue to believe that if oil can ever find rock bottom, and/or stabilize in a trading range, or start to appreciate, that there will be some major opportunities in the energy sector in equities, and in their high yield fixed income; Also I believe that when oil stabilizes (or begins to appreciate) that there will be some major opportunities in high yield fixed income funds, such as the ones listed above, EMB, PCY, HYG, JNK, and QLTC.

The US Dollar traded slightly lower versus the Euro on Thursday, the Euro gained approximately +0.30%. I continue to believe the Ruble and the Euro are still too high, and will further deteriorate, making the dollar stronger. Check up on current cross rates here: http://finance.yahoo.com/currency-investing/majors.

I believe the catalysts for today’s stock market rally were the economic data releases. Labor force figures exceeded expectations. Initial claims came in better than expected, at 265k, the prior figure was 308k, and consensus estimates were for 301k. Additionally, Continuing Claims came in at 2,385k, the prior figure was 2,456k, and consensus expectations were for 2,429k. Pending home sales came in at -3.7%, the prior figure was +0.6%, and consensus expectations were for +0.6%. Most believe that it was slightly light due to the Holiday of MLK which halted mortgage and banking activity this month.

Today, Bill Gross “the King of Bonds,” released his monthly commentary on the markets. He believes that higher rates will not be terrible for fixed income or for equities. You can read his report here: https://www.janus.com/bill-gross-investment-outlook, this month he talks of the board game Monopoly, and how his mother taught him how to play the board game. He mentions he likes orange and red properties rather than Boardwalk and Park Place. More seriously, Gross mentions that the U.S. recovery since the 2008 “greater depression” (as I like to call it) has been very weak and “anemic” as he says; Bill Gross also says he believes The FOMC will raise rates in late 2015. I’d counter that, the rebound hasn’t been a total flop, and at least stock market performance (as well as the high yield fixed income sector) has been absolutely stunning(!!!) over the past 5 to 6 years, off the rock bottom prices reached around March 9, 2009. I’d suggest no six year period will see +200% or greater stock index gains again, for quite a while (as we’ve all seen since March of 2009). Gross then goes on to discuss Dr. Francis Fukuyama’s estimates (read about Fukuyama here: http://en.wikipedia.org/wiki/Francis_Fukuyama) as if we know what he’s talking about. I believe Gross is pleased at the current risk of slight deflation and disflation, and currency strength, rather than run away inflation, and currency depreciation; perhaps this is what Dr. Fukuyama has projected in the past. It’s easy to project and estimate a reflationary environment and higher inflation rates, when inflation rates, and interest rates are at historical lows. There have been many Dollar bears in the past as well, due to the current account deficit; Especially the federal budget deficit in the USA. It’s kind of like saying there’s going to be a storm when the weather is beautiful, or vice versa.

I believe tomorrow the economic data releases may sway the market. I believe S&P Futures vs. Fair Value will be meaningless until the GDP release, which will make an impact. Gross Domestic Product (GDP) is expected to come in at +3.2%, the prior quarter was +5.0%; and the Chain Deflator-Advance is expected to come in at +1.0%, and the Employment Cost Index is projected to come in at +0.3%, also the Chicago PMI is expected to come in at 57.5, and lastly Michigan Sentiment is expected to come in at 97.5.

I’m still bullish on equities, for 2015, and for the near future. I continue to believe (as I’ve said earlier) that the stronger dollar and weakening oil prices will bode well for consumer sentiment and for consumer spending, which is the largest component of GDP. I think also a strengthening U.S. dollar, weaker inflation (aka disflation), and a weakening global economic outlook will result in the Federal Reserve raising rates at the earliest this summer, or perhaps closer to September, if not until later until perhaps in 2016.

In other news, MSFT finally saw some relief, after selling off strongly for a few days in a row, it was up 1.99% today. MCD had its CEO resign, and shares rose +5.06%. PCLN broke 1,000 per share trading downwards in the morning, before rallying to close up +11.49 to 1,014.74. PCLN hasn’t seen $1,000 per share for years. PCLN struck a high around March 5, 2014 at 1,370 per share. QCOM released EPS recently and traded downwards by -10.28% finishing the trading session at 63.69. BABA also traded down slumping by -8.78% to 89.81. GOOGL released its EPS after the closing bell, and missed the 7.11 EPS estimates, and was light on revenue. Tomorrow’s GOOGL performance will be interesting to examine. Shares initially sold off on the news, later however, shares are actually trading higher, and shares are up +7.77 in afterhours trading to 521. In “Big Oil” CVX reports EPS before the opening bell Friday. Friday’s EPS reports will also include LLY before the open, and SPG before the opening bell as well. In politics, President Obama asked the people and the Congress to approve a major spending increase for the U.S. Military. I believe this is a mistake, only because as a nation we spend more than 10 times (on our military budget) then the rest of the entire world’s defense budgets summed together; this is not an exaggeration. I worry about major budget deficits fueled by higher and higher (and rapidly growing) defense budget expenditures. I’d like to see a U.S. President raise the defense budget by about +0.001% annually (despite any inflation possible that may or would materialize) for at least the next two terms of presidency in the United States. That would likely be beneficial to the U.S. economy, and may allow for increased growth rates and increased economic development & activity. I may not even be opposed to a future President that may decrease the Department of Defense Budget. We need a President who can manage to balance the budget, or better yet, one who can run a surplus.

S&P Futures vs. Fair Value are indicating Friday’s implied open will be nearly unchanged (click here for a futures update).

By Andrew G. Bernhardt