On the Securities Action of Wednesday, February 4, 2015

“SLIGHT SELL OFF ON WALL STREET!”

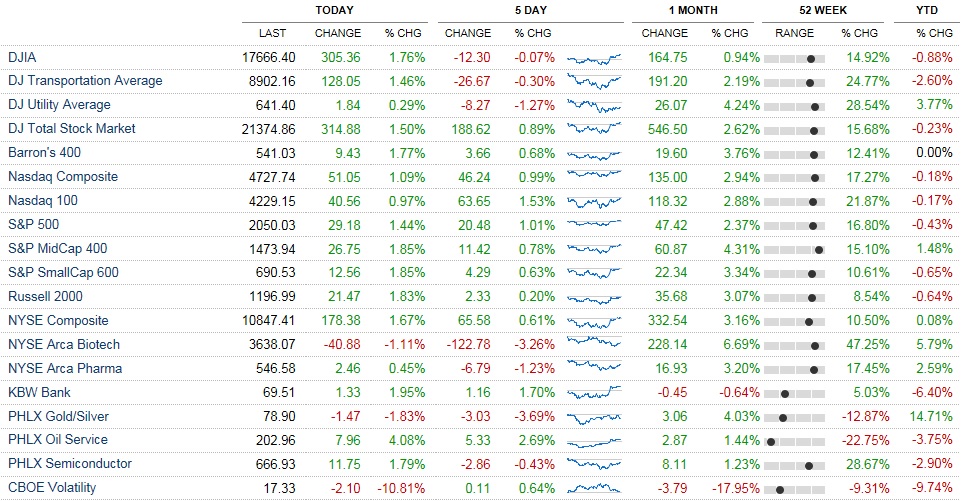

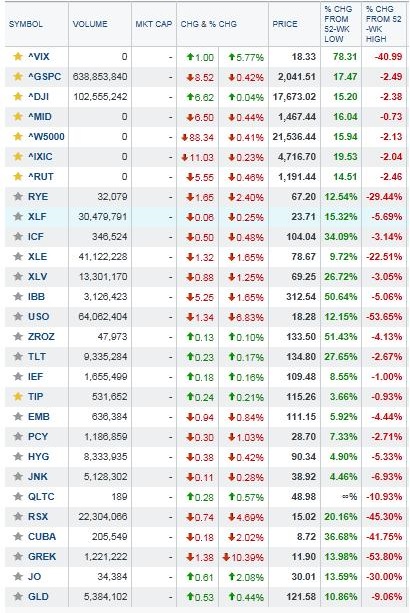

Slight sell off on Wall Street! Wednesday saw most major U.S. stock indices down by -0.20% to -0.40%. Volatility, as measured by the VIX rose +5.77% to 18.33. The S&P500 finished -8 points to 2,041, the DJIA was up +6.62 points to 17,673. The S&PMidCap400 declined -0.44% to 1,467. In fixed income, Treasuries traded higher, while high yield sovereigns and BB-rated high yield corporate debt traded lower; CCC rated fixed income saw price increases. I believe the major U.S. stock indices will soon plow through previous all time highs, by three to four percent, before taking a few steps back, before making another advance higher. I continue to remain bullish, and I believe energy shares and crude oil will trade in a volatile range, but will trade higher given a month or two or more, which I believe will lift all major U.S. Stock Indices to new highs.

Feb. 4, 2015, Major U.S. Stock Indices

Select Quotes of Interest, Feb. 4, 2015

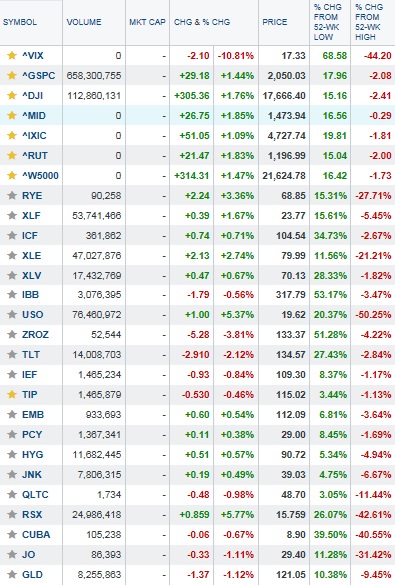

[http://finance.yahoo.com/futures] Click here for an energy prices update] Tuesday saw USO an etf of West Texas Intermediate decline by -6.83% to 18.28; This was a reaction to oil inventories data, that came in at nearly 80 year highs! This according to the EIA. I believe oil will remain very volatile; It settled at 48.61 per barrel (down -8.70%) on Wednesday.

In the Fixed income markets, see the graphic above to see how Treasury etfs traded (ZROZ, TLT, IEF, TIP) and how high yield etfs traded (EMB, PCY, HYG, JNK, and QLTC). The 30 year Treasury yield closed at 2.39, and the 10 year Treasury Note yield closed at 1.89 [data from here: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield. I continue to believe, and will reiterate, that if oil can stabilize in a trading range, or start to appreciate, that there will be some major opportunities in the energy sector in equities, and in their high yield fixed income; Also I continue to believe that when oil stabilizes (or begins to appreciate) that there will be some major opportunities in high yield fixed income funds, such as the ones listed above, EMB, PCY, HYG, JNK, and QLTC.

The US Dollar traded higher versus the Ruble and the Euro on Wednesday; the Euro lost approximately -0.81%, as measured by the etf FXE. GM also released its eps report on Wednesday morning; it handily beat expectations, and shares rose by +5.44% to 35.83. I continue to believe the Ruble and the Euro are still too high, and will further deteriorate, making the dollar stronger. The U.S. Dollar can now be exchanged for a Euro at a cost of approximately $1.1354, and also can now be exchanged for 67.8995 Rubles, which is about two point eight Rubles and change more than yesterday. [http://finance.yahoo.com/currency-investing] Go here for an update on all major cross rates.

I believe the catalysts for today’s stock market loss were predominately lower oil and energy prices, as well as Greece sovereign debt pessimism increasing as Europe told Greece it could not back its bank debt with its sovereign debt as collateral; Consequently, shares in Greece fell on their exchanges, and in the USA, an etf of Greek stocks etf ticker GREK, declined by -10.39% to 11.90. I also believe that oil could prove to be very volatile; so perhaps an option strategy called an at-the-money straddle could be lucrative when choosing expirations about two weeks away.

Economic data releases on Thursday the 5th will see Initial Claims, the Trade Balance, Productivity, Unit Labor Costs, Natural Gas Inventories, Payrolls, the Unemployment Rate, Hourly Earnings, Average Workweek, and Consumer Credit economic data releases.

In notable eps reports releases I had speculated yesterday that CMG would be amusing, as would WYNN. Both eps reports were released after the market close on Tuesday the 3rd. I had said that CMG may move by ±51.00 on Wednesday, during the full trading day after it reports eps. Wednesday the 3rd saw CMG decline by -50.63 or -6.97% to 676 per share, and WYNN declined by -9.69 or -6.22% to 146.11 per share. I had suggested that perhaps a long bull call ratio back spread with net credit characteristics may be lucrative; Especially if also combined with a long bear put ratio back spread with net credit characteristics on CMG, placed today just a minute or two before the close (3:00PM Central Time) on February 3rd could prove to be lucrative. It certainly was amusing to see what happened Wednesday.

I continue to believe that long bull call ratio back spreads with net credit characteristics, initiated simultaneously with long bear put ratio back spreads with net credit characteristics (initiated just minutes before the closing bell) could prove to be a very lucrative trading strategy, when focused on “HYPE(!!!) stocks just prior to their eps releases. Up and coming hype stock eps releases include TWTR, YUM, and LNKD. Happy earnings speculation!

I will reiterate that I’m currently bullish on the major U.S. stock indices, despite S&P Future vs. Fair Value currently indicating that Thursday may see stocks open down by -67 points. I believe a theme of higher crude oil prices will potentially materialize over the next few weeks, if not becoming more of a longer term theme, for the next year, if not longer. I also believe that the geopolitical risks involving Greece’s sovereign debt and interest payments will be resolved, and that Russia may stop sabre rattling soon. This will bring about higher prices for stocks, and for all major U.S. stock indices, which could reach new all time highs very soon. I also think that investors may begin selling longer duration and longer maturity fixed income of all kinds, and with the proceeds they may purchase stocks, resulting in higher yields on fixed income, and also higher stock prices. Interestingly, I believe that the higher credit quality fixed income may sell off more than the lower credit quality fixed income. I would base this upon the unprecedented sovereign yields worldwide and in the USA. High yield fixed income yields are not at all time lows, but e.g. Treasury yields are at nearly all time lows. To me this means that Treasuries at the long end, may suffer greater losses on a percentage basis versus their high yield counterparts. For 2015 I am most bullish on equities within the Financials, REITs, and “Big Tobacco” sectors; In fixed income I like high yield etfs e.g. EMB, PCY, JNK, HYG, and QLTC. I’d likely trade deep in the money calls on stock indices, combined with high allocations to high yield fixed income. Happy trading!

By Andrew G. Bernhardt