On the Securities Action of Friday, February 6, 2015

“WEEKEND UPDATE- SLIGHT SELL OFF ON BROAD & WALL”

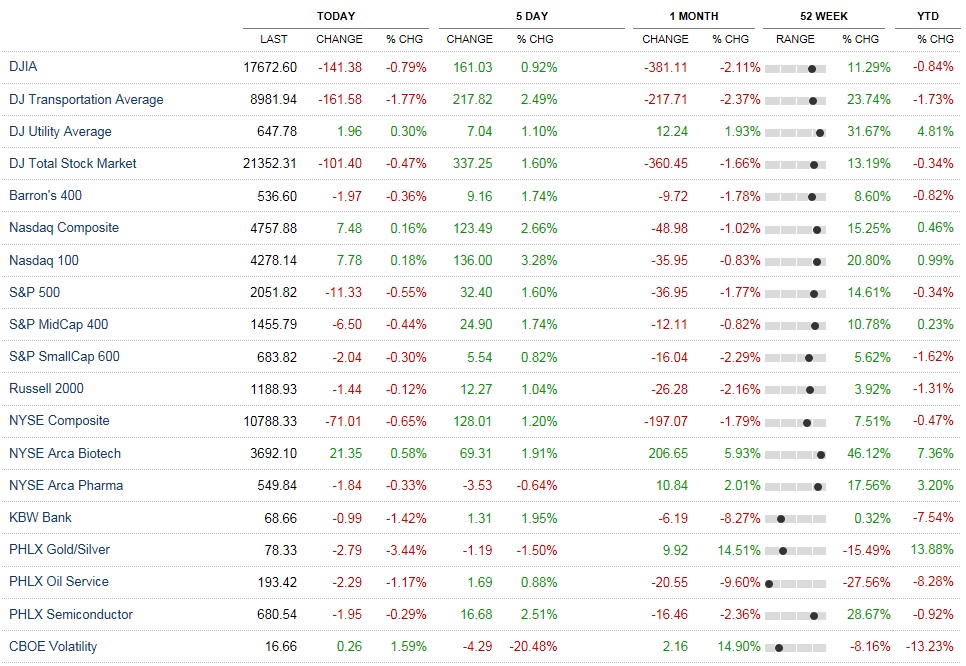

SLIGHT SELL OFF ON WALL STREET. Friday saw most major U.S. stock indices decline by about -0.30%. However for the week, the DJIA gained +3.84%, the S&P500 gained +3.03%, and the S&PMidCap400 gained +2.91%. The indices finally got themselves into positive territory for the YTD figures as well. On Friday, volatility, as measured by the VIX increased by +0.44 points or +2.61% to 17.29. See the graphic below for daily and weekly performance of the U.S. Major Stock Indices. In fixed income Friday, Treasuries traded lower, as did high yield Sovereigns, while high yield corporates rallied. See the graphic below to see how fixed income faired Friday. I continue to believe the major U.S. stock indices will soon plow through previous all time highs, by three to four percent, before taking a few steps back, before making another advance higher. I continue to remain bullish, and I believe energy shares and crude oil will trade in a volatile range, but will trade higher given a month or two or more, which I believe will lift all major U.S. Stock Indices to new highs. Lastly, I think that higher energy prices will bring “hot” (meaning higher than usual) CPI-U monthly figures, which will put upward pressure on fixed income yields in the open market, particularly in the Treasury long term and intermediate maturity sectors. The average monthly CPI monthly increase has been approximately +0.2%, since oil’s “demise” it’s been quite low, closer to zero, if not negative month to month. As energy prices (primarily light sweet crude oil) rebounds, I’d expect the monthly CPI-U figures to come in “hot” at nearly twice to three times the historical average, at literally +0.4% to +0.6% month to month for a while. Treasuries are just off prices of nearly unprecedented highs, due to unprecedented low yields. Thirty year zeros are down by -8.61% off their all time highs, which I believe they’ll never see again, or at least, for many many years. Conventional thirty year Treasury bonds are down by -5.44% off of their peak. Long term (and intermediate) treasury yields have no where to go but upwards, which will bring Treasury prices down further, due to higher yields. High yield fixed income is not at unprecedented low yields, and therefore, may not sell off as strongly as Treasuries, given equal maturities. Higher or “hot” CPI-U monthly figures could also put pressure on the FOMC to raise rates, perhaps as early as this summer. Higher yields at the short end (raised by the Federal Reserve) are likely to push rates up across the board. I wouldn’t be surprised if long term Treasury Securities saw negative total returns over the next 36 months. I believe, long term maturity Treasury bond investors (and perhaps intermediate Treasury note investors) are in for a big surprise(!!!), called negative total returns over the next three years, as rates begin to “normalize” in the USA. I believe investors will be totally shocked at how much can be lost in a Treasury bond as rates increase. If rates rise by 200 basis points at the long end, there could literally be 30% losses for Treasury bond investors. Additionally, there could be nearly literally 60% losses for 30 year Zeroes in the Treasury Bond market. Interest rate risk is measured by duration. Swim at your own risk!

Feb. 6, 2015, Major U.S. Stock Indices

[http://finance.yahoo.com/futures Click here for an energy prices update] Friday saw USO an etf of West Texas Intermediate increase by +2.31% to 19.47; USO is now -50.61% off its peak of the past 12 months; reached in late June ’14; USO is also +19.45% off rock bottom, set on January 29th at 16.68. I believe oil will remain very volatile, perhaps an options strategy called an at-the-money straddle using two week out expirations could prove to be very lucrative; I believe oil is going a lot higher (maybe another 10% or more), and soon (over the next few weeks). I would base this estimate of mine on the oil-VIX which is extremely high right now. If the oil-VIX implodes, it will bring higher oil prices. On Friday light sweet crude oil traded higher by +3.68% or 1.86 per barrel to $52.34. Higher oil likely sent the Russian stock market (as measured by the etf RSX) up by +3.29% to 16.34; RSX now stands -40.50% off its peak of the past 12 months. [Click here for an Oil-VIX chart & update]

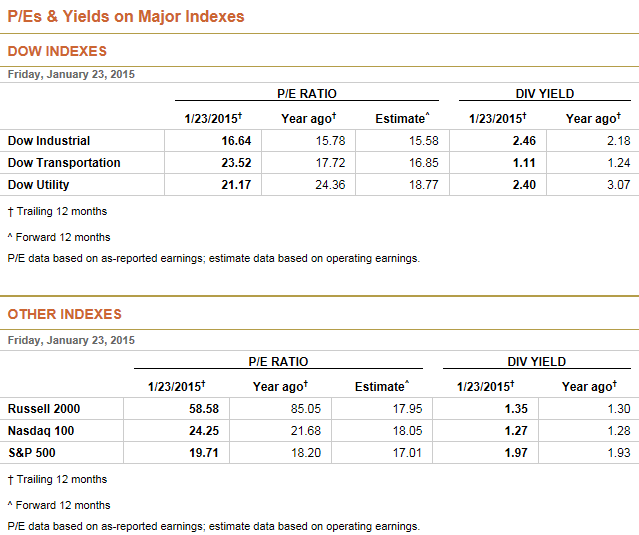

PE Multiples & Yields of Major U.S. Stock Indices, Feb. 6, 2015

As you can see the PE Multiple of the DJIA is just 16.78, it was 15.08 last year; The dividend yield of the DJIA is 2.45%, and it was 2.49% last year. The 30 year Treasury bond yield is 2.52%,and the ten year Treasury note yield is 1.94%. Therefore, it’s difficult to be bearish on the equities markets with a stock market with a lot of potential to go higher. [Click here for Yields on Treasury Securities, http://finance.yahoo.com/quotes/^IRX,^FVX,^TNX,^TYX]

Select Quotes of Interest, Feb. 6, 2015

In the Fixed income markets, see the graphic above to see how Treasury etfs traded (ZROZ, TLT, IEF, TIP) and how high yield etfs traded (U.S. dollar denominated high yield sovereigns being etfs EMB and PCY) (as well as high yield corporate fixed income being etfs HYG, JNK, and QLTC). The 30 year Treasury Bond yield closed at 2.51%, and the 10 year Treasury Note yield closed at 1.95% [Data from here: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield]. I continue to believe, and will reiterate, that if oil can stabilize in a trading range, or start to appreciate, that there will be some major opportunities in the energy sector in equities, and in their high yield fixed income; Also I continue to believe that when oil stabilizes (or begins to appreciate) that there will be some major opportunities in high yield fixed income funds, such as the ones listed above, EMB, PCY, HYG, JNK, and QLTC. When higher energy prices materialize in the future, inflation could pick up as measured by the CPI-U, which may or could send e.g. Treasury Security yields higher, while also pressuring the FOMC to raise rates at the short end.

Friday saw the US Dollar trade lower versus the Ruble, but significantly higher versus the Euro; The Euro lost approximately -1.47%, as measured by the etf FXE. I continue to believe the Ruble and the Euro are still too high, and will further deteriorate, making the dollar stronger. The U.S. Dollar can now be exchanged for a Euro at a cost of approximately $1.1315, and also can now be exchanged for 66.5245 Rubles, which is about -0.25 Rubles less than yesterday’s exchange rate. [http://finance.yahoo.com/currency-investing Click here for an update on all major cross rates.]

I believe the catalysts for today’s stock market declines were higher oil and in-line labor market figures, which indicated a very strong labor market. A stronger economy means that the Federal Reserve may raise rates sooner rather than later. This threw cold water on the markets mid-day, turning slight gains to slight losses by the closing bell; Higher oil prices lifted the energy sector; Lastly, shares in Greece lost ground as pessimism increased. Consequently, an etf of Greek stocks (etf ticker GREK) declined by -4.59% to 11.85.

Above is a summary graphic of the weeks economic data releases.

[Click here for updates on Futures vs. Fair value, http://www.cnbc.com/id/17689937].

Monday before the opening bell and after the opening bell will not see too many hype stocks report eps. HOT and Z will both report eps Tuesday after the close. I believe that Z could move about ±6.80 per share after it reports its eps, it closed Friday at 100.65.

I would suggest that perhaps a long bull call ratio back spread with net credit characteristics may be lucrative; Especially if also combined with a long bear put ratio back spread with net credit characteristics on any particular “hype stock” just before eps are released; Placing the trade just a minute or two before the close (3:00PM Central Time) on its earnings release date (if it reports that day after the close, or the next morning before the opening bell). It certainly is amusing to see what happens to hype stocks just after their eps releases in the aftermarkets and on the first full day of trading post eps. Most sink fast!

“Hype stocks” to me would be e.g. GOOGL, TSLA, PCLN, FB, AAPL, LNKD, AMZN, EBAY, NFLX, TWTR, BABA, GPRO, and Z, and also what I would describe as “Big Momentum Players” such as e.g. CMG, GMCR, AZO, V, and MA etc. (a sub group of hype to me). This list of Hype and Big Momentum Players is just off the top of my head, and is in no particular order, nor is it any particular science for choosing these types of volatile securities. RSX, GREK, TUR, FXI, EWZ, and CUBA are also very volatile etfs found in places worldwide with high geopolitical risks. West Texas Intermediate matched by the etf USO is also a very volatile etf to trade as of late.

I will continue to reiterate that I’m currently bullish on the major U.S. stock indices. I believe a theme of higher crude oil prices will potentially materialize over the next few weeks, if not becoming more of a longer term theme, for the next year, if not longer. I also believe and would reiterate that the geopolitical risks involving Greece’s sovereign debt and interest payments will be resolved, and also that Russia may stop sabre rattling soon. This will bring about higher prices for stocks, and for all major U.S. stock indices, which could reach new all time highs very soon. I also think that investors may begin selling longer duration and longer maturity fixed income of all kinds, and with the proceeds they may purchase stocks, resulting in higher yields on fixed income, and also higher stock prices. Higher energy prices may bring about higher monthly CPI-U inflation figures, resulting in a fixed income sell off, and higher interest rates, over the next 6 to 12 months, if not for the next 36 months. Interestingly, I believe that the higher credit quality fixed income may sell off more than the lower credit quality fixed income. I would base this upon the unprecedented sovereign yields worldwide and in the USA. To me, this means that Treasuries at the long end, may suffer great losses as rates “normalize.” For 2015 I am most bullish on equities and the S&PMidCap400, the S&P500, as well as the DJIA. The DJIA has the lowest PE Multiple among all the major U.S. Indices currently. I am also bullish on Financials, REITs (particularly Hospital REITs such as HCP, HCN, SBRA, OHI, NHI), and the “Big Tobacco” (e.g MO, PM, RAI, BTI, etc.) sectors; In fixed income I like high yield etfs e.g. EMB, PCY, JNK, HYG, and QLTC. Options can be used to “hedge” fixed income ETFs as well, in strategies such as level one covered call writing (of e.g. at-the-money monthly calls). I’d likely trade deep in the money calls on stock indices, combined with very high allocations to high yield fixed income. If the JPM EMBI (matched by etf ticker: EMB) is good enough for the fixed income of the Yale and Harvard Endowment funds (and other large time institutional entities) then why trade Treasury Securities? I think people (or any entity) who buy Treasuries are “ripping themselves off!” Treasuries to me, generally speaking are for short term investing, and maximum preservation of capital. All high yield fixed income indices (which are BB rated) have, over the long run, always closed at a new all time high every 18 rolling month period. Consequently, every or any time that high yield fixed income indices are trading well off their all time highs, I’d view it as a major buying opportunity! Happy Trading!

By Andrew G. Bernhardt