DEEP THOUGHTS ON THE SECURITIES MARKETS AND THE ECONOMY

It’s been the worst start for a year… Ever.

Do you know what I think of the most recent stock market sell off? I think it’s phony as hell! There is literally no catalyst I can think of that sparked the most recent sell off. So, in my mind, there could easily be a strong snap back rally, like in late August and September, etc.

When I think about “crisis watch,” “crises watch,” or “bubble(s) watch,” a game I play with myself and with the old wise men I know and trust, I (and we) can’t think of any valid issue looming to spark further selling. In my mind, the recent sell off has been completely and utterly irrational and illogical. Know that it can “get worse,” before it “gets better.”

Why are the indices 10 to 15 percent off their peaks? Why does everyone literally sell everything indiscriminately on low and lower oil?! Low and lower oil is great for the U.S. economy (it’s only “bad” for OPEC nations, and bad for the energy sector). It’s bad for Brazil, Russia, Saudi Arabia, Iran, Iraq, and Kuwait. In the USA the entire energy sector is allocated into the broad based indices around 2.59 percent to 6.4 percent. So, the energy sector is really a tiny sector of the US economy, and is a tiny allocation to its broad based stock indices. Let the whole f-ing sector go bankrupt due to its own inept incompetence and ignorance of total overproduction!

When I see oil trading lower (nearly every day now), I think “great” and also “the market should be surging!!!” The USA isn’t Kuwait or Saudi Arabia, it’s not Brazil or Russia either. I worry investors believe it is! Why have the broad based indices correlated to the trajectory of oil over the last couple months?! Oil has been going down for 8 to 9 years now! It peaked above 145 per barrel. Low and lower oil and energy prices are great for the U.S. economy because it’s like a tax cut, and it stimulates consumer spending and consumer sentiment, which are major components and drivers of GDP growth. There is literally no recession looming in our immediate future for the USA, not in 2016, and likely not in 2017 either. GDP growth is expected to accelerate worldwide, except for China which claims recently it has decelerated to just +6.5 percent GDP growth expected for 2016. There is no looming housing market collapse, there is no massive layoffs around the corner, and unemployment is low, and the labor market is strengthening. Additionally, real estate in the USA is also strengthening; It and REITs will not be highly damaged by interest rates going from zero to 25 basis points, or even if rates reached 1.25 percent, or even 4 percent. Even 3.5 to 4.0 percent fed funds is “accommodative.” Inflation is under control, and is very low, which should be great for PE expansion. Maybe in the next year it will reach a CPI-U of +2.0% to +2.5%. Interest rates have finally begun to rise, off of zero, and stand at 0.25 percent. Janet Yellen at the Fed is expected to raise rates to 1.00 to 1.25 percent by early 2017.

There is no boogey man coming for the markets, instead the markets just might boogey woogie higher!

Beware of the angry bull’s threat display!

Alternatively, if the markets continue their downward trend, I’m not sure what everyone will blame the nasty bear market on, if one materializes? Did the economic cycle die of old age? Was it paralyzed by interest rates reaching perhaps 0.75% in the future? Was it King Dollar, and the emerging market currency depreciation? Maybe investors worldwide are worried about extensive U.S. tax reform? Perhaps, there is political risk? Would “The Donald” or “Hill & Bill” really be that bad for our futures?! Do you think anything they even claim they will do will be done? Either of them doing anything will be met with total resistance and nothing they want will happen; So, nothing will change. Know usually though, election years are great for investors, and just because the markets completely fell apart during the last election doesn’t mean it will this time! It was a total coincidence to me during the last election that the markets imploded. The markets implosion from late 2007 through early 2009 was directly associated with the housing market bubble, reckless lending (the “NINJA LOANS” – no income, no job, and no asset loans), and too many fools (with terrible credit quality) who owned homes, who couldn’t afford it- especially once the economy went from boom to bust. There is no parallels today, to that reckless past of ours. Banks nearly don’t do anything, exceptchecking and savings accounts, they nearly never lend anymore, and they are and have been regulated the f-ing hell out of; So, there’s no bad loans to go bust. The future is bright.

Who cares about the “bubble” popping (in its final stages) in China in its stock market?! The Chinese markets are already down more than fifty percent! The Chinese markets have not appreciated now for many many years, they’ve really been rolled back. How many bubbles in emerging market stocks have there been in the past 15 to 25 years?! It’s not the first or the last time there’s an emerging market collapse. I’ve said for years, emerging market stocks are like lotto tickets! Furthermore, who really cares about North Korea’s nuclear weapons testing?! Every country has tested nuclear weapons. Nuclear weapons have been around since the end of WWII, and I’m sure every country that wants them, has them; Its been over 70 years since they were first invented and designed, and unfortunately they’re very cost effective and cheap. The USA blew them up running tests constantly in the ’40s, ’50s, and ’60s (probably up until the nuclear test ban treaty in the mid to late ’90s!), under water, at sea level, and above sea level, underground too, and also at very very high altitude (which disgustingly and mysteriously knocked out all radio transmission signals worldwide for several hours).

To me the fear mongering, war mongering, and terrorism discount on the markets has been overdone. The pessimism, the fear, and paranoia over nothing has been overdone. Volatility is very elevated to me.

At some point sanity will return.

The only risk I see lately, is that the perception is that higher rates will increase the value of the U.S. dollar against the euro, and also especially against emerging market currencies, reducing our exports, leading to a drag on sales volumes, and also on foreign earned income. The ruble has been particularly weak, china has been artificially depreciating its currency the yuan aka the renminbi. Brazil is having its worst recession in at least 30 years, thanks to low and lower oil, and rapidly depreciating commodities like coffee, and sugar, etc. Brazil is also plagued by low prices for iron, juices, cars, petroleum, tobacco, soy beans, poultry, and meat. At some point, Brazil is going to be a fantastic opportunity for investors. It like Russia, will likely reach rock bottom, once oil hits rock bottom.

When will oil hit rock bottom?! It’s anyone’s best guess, but I think we’re getting close, and it’s likely at some point in the next 2 to 4 months. Oil can’t decline substantially every day, forever. Oil, energy, and basic materials will likely represent a huge opportunity for investors as well, once oil hits rock bottom.

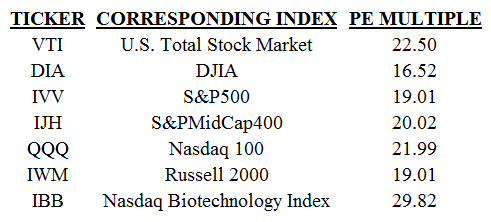

I believe the future is bright, and despite the worst start for any year, I still believe that the U.S. broad based stock indices (matched by tickers: VTI, DIA, SPY, MDY, and maybe IWM) represent the best investments for long term (10+ years) investors. I also really like tickers EMB and PCY (which match the U.S. dollar denominated JPM EMBI), and over the long run, over every 24 months or greater, I believe that these tickers will provide positive total returns.

I think it’s time to be bullish. There’s a small chance of total idiocy and paranoia and a huge market sell off, to a depth of maybe -30 to -40 percent off the all time highs of the broad based stock indices, but with no valid or logical or rational catalyst, I really don’t see that happening, until there is actually a recession. I firmly believe that there is no recession looming (anytime soon) in the USA (not in ’16 or ’17), so I see no reason for a bear market materializing.

The grizzly bear can’t even believe it this time!

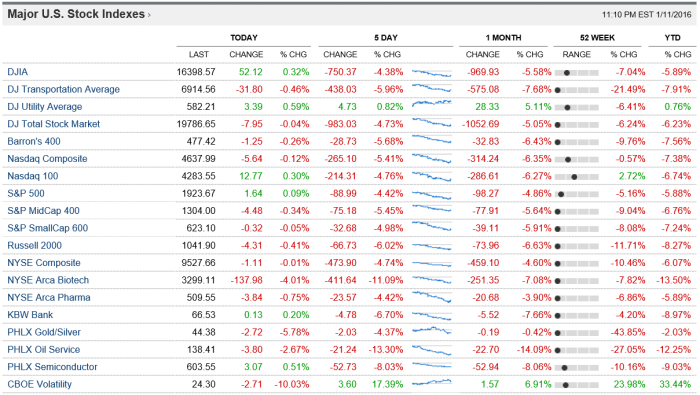

Here are some reports to use, to assess the economy of the USA and the world.

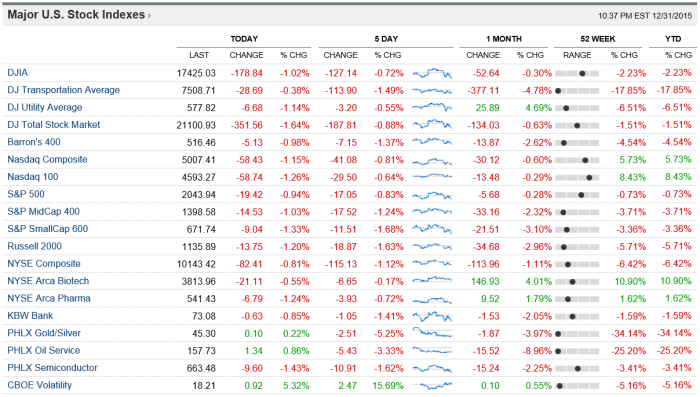

Data retrieved and compiled 12-31-15 (after market close)

Through 12-31-2015 (at the close)

As you can see, today, this week, this month, and spanning over the past 12 months has been a disappointment for equity investors.The only bright spots have been the Nasdaq (ticker ONEQ +5.93% YTD) and the Nasdaq 100 (ticker QQQ +8.43% YTD), and Biotech (tickers IBB +11.47% YTD, and XBI). The Cohen & Steers Realty Majors Index, matched by ticker ICF, posted a +5.96% return in 2015. Additionally, U.S. Total Stock Market Index, formerly known as the Wilshire 5000, (ticker VTI) posted +0.40% YTD. Winning sectors in the S&P500 (which finished 2015 -0.73%) included Technology Sector (ticker XLK), Health Care (ticker XLV), and Consumer Discretionary (ticker XLY), and Consumer Staples (ticker XLP).

Click here for quotes on the ticker SPY, and all of the SPDR Sector ETFs which match the performance of the sectors constituting the S&P500.Here’s how some indices and sectors and their ETFs did for 2015, ranked in order, from biggest winners to biggest losers (results were taken from a price chart, so this includes price performance only, not including dividends, and also does not include capital gains distributions):

IBB the Nasdaq Biotech Index, a widely followed sub-sector of health care wins first place.

QQQ, the Nasdaq 100, wins second place.

XLY, Consumer Discretionary wins third place.

XLV, Healthcare, wins fourth place.

XLP, Consumer Staples, wins fifth place.

XLK, Technology, wins sixth place.

The S&P500 itself finishes for seventh place, down for the year.

DIA, the DJIA finishes down for the year, in eighth place.

IJH and MDY, the S&PMidCap400 finishes down for ninth place.

IWM, Russell 2000 finishes worse, down for the year, and in tenth place.

XLF, Financials, were next, finishing down for the year, in eleventh place.

XLI, Industrials were next, finishing down for the year, and in twelfth place.

XLU, Utilities, were next, finishing down worse still for the year, and in thirteenth place.

XLB, Basic Materials, finished down, second to last, in fourteenth place.

XLE, Energy, finished down and in last place, fifteenth place. (And after being down so sharply over the past 18 months, something tells me that the energy sector could prove to be a winner going forward, at maybe some point between now and the next six months or so.)

Worse still were many foreign stock ETFs, of Europe, the Middle East, China, India, Brazil, The frontier markets, South Africa, Africa, S.E. Asia, Latin America, etc. (click here for quotes on these losers), know that it can always get worse before it gets better, so don’t be too tempted to buy these foreign stock ETFs. I’ve always said foreign stocks are like gambling and/or lottery tickets! Now there’s always exceptions to what I’ve said, e.g. I like CS, DB, GSK, MNK, BCS, and LYG, which are all foreign domiciled “big pharma” and financials. On that note, checkout ETF ticker ADRU, which is laden with foreign companies (mostly ADRs listed in the U.S.) that might maybe be worth an investment.

There are three strategies that can be put into action on the last day of the year, the first is called “The Bridesmaid Strategy,” second, “The Dogs of the Dow Strategy,” and lastly, the third, “The Small Dogs of the Dow.”

1. The Bridesmaid Strategy is simple, you simply select the 2nd place winner among all S&P500 sectors, which is healthcare for 2015, and you invest solely in that sector for the following year, being 2016. This strategy is said to beat the S&P500 by over four hundred and eighty basis points (meaning by +4.80%) per year on average, over the long run. So, 2016’s Bridesmaid Strategy would entail investing in the S&P500’s Health Care Sector, matched by ETF ticker XLV.

For further info on “the Bridesmaid Strategy” click here. The article claims The bridesmaid strategy has an annualized return of +14.50% since 1991, and over that same span (since 1991) the S&P500’s annualized return was +9.70. Seems as though the bridesmaid strategy is absolute dynamite!!!

I’d also note that biotech (which is not a sector of the S&P500, it’s its own index), matched by the ETF ticker IBB, and other healthcare related ETFs could prove to be great investments in 2016, see tickers IHE, XPH, SBIO, and others.

Know that despite the health care sector’s strong performances over the past few years, like everything else, past performance is not indicative of future performance, and does not guarantee future results.Swim at your own risk!

2. Also, Click here for 2016’s Dogs of the Dow Components. Click here for an explanation on how (A) the Dogs of the Dow (and (B) the Small Dogs of the Dow) are selected. It’s really a great time tested strategy. The Dogs of the Dow strategy involves selecting and investing in an equal weight 10% allocation, the 10 highest yielding stocks taken out of the DJIA (on the last trading day of the year); The Small Dogs of the Dow Strategy then chooses only five (out of ten) from that list, in equal weight (20% each), which are the lowest in price per share.

Leading the way down in 2015 was the energy sector (XLE) (and iShares ticker IYE, -22.21% YTD), plagued by sharply declining crude oil prices, from too much supply, rather than lack of demand. Their man made supply side shock could put them out of business, and has also caused terrible recessions in Brazil (in 2016 many believe Brazil could turn, and ticker EWZ (-41.27% YTD) could prove to be a major opportunity for speculators, after nearly 8 to 9 years of steep declines!), terrible recessions in Russia (ticker RSX -0.56% YTD), and troubles in Turkey (ticker TUR, -31.46% YTD), Saudi Arabia, and Kuwait, etc. Basically, OPEC is too productive.There could be nasty times ahead for the energy sector still (and for OPEC nations), even after 18 months of steep declines in oil prices (coming off of 104 per barrel in 2014, to the current 37.04 (for WTI; and 37.28 for Brent) [oil prices retrieved from here, oil-price.net] per barrel on December 31, 2015). Oil peaked in July of 2008 at just over $145 per barrel [click here for that chart], so its been declining for eight years now. There could be easily be consolidation, further layoffs, the slashing of dividends across the board, many bankruptcies, and general doom and gloom for the entire energy sector. In addition to a very weak energy sector, joining in on the way down, and putting negative pressure on the S&P500 was its sectors including basic materials (XLB), utilities (XLU), and industrials (XLI). Despite lower oil prices, the Dow Jones Transportation index finished down by -17.85% YTD (ticker IYT finished 2015 down by -16.85%).

In addition to ticker EWZ, there may be some great opportunities in the S&PLatinAmerica40 index, matched by ticker ILF (-31.40% YTD). Additionally, I like to follow the performance of ticker IDV as well, “the International Select Dividend ETF” by Blackrock’s iShares, which posted losses of -10.92% in 2015; and IXG (-4.40% YTD) the iShares Global Financials ETF; and ticker EUFN (-4.99% YTD) the iShares MSCI Europe Financials ETF. Check them out!

Somehow, I’m still bullish for 2016, as I see lower and low oil prices acting like a tax cut, which is good for consumer sentiment and consumer spending.Low and lower oil is great for the U.S. economy.Also, the entire energy sector represents only 2.59 to roughly 6.5% of all the U.S. broad based stock indices (just 3.03% of the S&PMidCap400, matched by ticker MDY and IJH).

Sometimes I wonder if too many believe that the USA is a very very oil intensive nation. We’re not, and we’re certainly not Kuwait, Saudi Arabia, Russia, or Brazil. I also worry that a lot of the selling “of everything” indiscriminately on low and lower oil (which is the trading action we’ve seen lately) is program trading, or algorithmic trading, or high frequency trading, and if so, eventually, they’re going to have to re-program their machines to interpret low and lower oil prices as beneficial and bullish for the USA and its stock markets, and inflationary outlook, and thus for fixed income prices and yields. Low and lower oil only hurts two things, (1) the energy sector, and (2) OPEC nations; It is absolutely fantastic for everyone else.

To me, I can’t figure out why so many are so foolishly bearish at this juncture, at mid-cycle, after the first rate hike off of zero interest rate policy. There is no nasty boogey man looming for the markets, in 2016 in my view. Instead, the market could really boogey woogey higher in 2016! I believe 2015’s performance was a little crummy due to that I describe as “a hang over” from 2013’s unusually strong performance, where many of the U.S. broad based indices rose over +30.00%. In 2013 e.g. the S&PMidCap400 rose by +31.57%, and the S&P500 rose by +29.60% (the S&P500 can be matched using the ETF ticker SPY), and the DJIA (matched by the ETF ticker DIA) rose by +26.50% in 2013. To me, it’s a shame that 2013’s thirty percent gain couldn’t have been spread out more evenly over the course of three years, in ’13, ’14, and ’15, everyone likes consistency.

High yield U.S. corporate junk bonds (and their indices, matched by the ETF tickers HYG (-5.54% YTD), and JNK) also didn’t do too well in 2015, they’re both down nearly five and a half percent, including their streaming income… on a price performance basis, they’re both down nearly ten percent); It has been odd in the sense that there is no recession in the USA, yet the junk bond market has posted a negative return. The negative sentiment about the energy sector’s fixed income has led to losses in high yield. Some are worried about many energy sector bankruptcies.

Personally, in the high yield junk bond sector, I like sovereign U.S. dollar denominated high yield junk fixed income, as is indexed by the JPM EMBI, matched by ETF tickers PCY and EMB. Click here for Payden & Rygel’s analysis on the JPM EMBI for this week. There is also the JPM EMBI Local Currency Bond Index, I really don’t recommend this foreign currency (aka “local currency”) denominated bond index. King dollar is back!

The markets in 2015 were also worried about slowing China (see tickers FXI -11.91% YTD, ASHR, ASHS, HAO -2.05% YTD, PEK -1.20% YTD), slow Europe (EFA -0.90% YTD), Greece (GREK -39.95% YTD) and its debt crisis, Puerto Rico’s debt debacle, and rising rates in the USA off of its zero interest rate policy (ZIRP), while the rest of the world has been and still is in rate reduction and stimulus mode. None of this was a surprise however, and many have been talking about these issues for years. China could also prove to surprise to the upside, and not slow as much as is widely believed. Additionally, there’s been worries about global and domestic terrorism, after the tragic events in Paris and California. I believe there is a terrorism discount weighing on the markets right now. Lastly, there could be worries about the political risks in the U.S. since 2016 is an election year, in what appears to be “the Donald” versus “Hill & Bill” (or really just Hillary). The republicans can’t seem to coalesce around any of their numerous candidates running for president; and the democrats apparently only have leadership from solely one candidate, Hillary.

In the USA, GDP is expected to expand at a faster pace next year, from approximately 2.50% in 2015, to roughly +2.7% to 2.8% in 2016. Inflation is expected to creep up, but remain low, maybe going from roughly 0.00% to 0.30% to roughly 1.50% to 1.75% percent in 2016. Additionally, I believe and expect the real estate markets in the U.S. will strengthen, and the U.S. labor market will strengthen as well. Interest rates are expected in the USA to go from 0.25% percent, to roughly 1.25% at the short end. On December 31, 2015 the 30 Year Treasury Bond yield currently rests at 3.02%, the 10 Year Note Yield rests at 2.27%, the Five Year Note closed at 1.76%, and the 13 week T-Bill Yield rests at 0.15%. I expect the yield curve to flatten slightly, but remain steep, as all rates should creep up a bit. Maybe the 30 year bond yield will increase 75 basis points in 2016, while the short end rises 100 basis points. We shall see. Globally, GDP is expected to grow worldwide, at roughly +3%. China is expecting roughly 6 to 7 percent GDP growth, S.E. Asia expects to see +4% growth. Even Europe is expecting to grow in 2016, at a faster pace than 2015’s sluggish growth.

(Chart #1) 12 Month Performance of the U.S. Broad Based Stock Indices(Chart #2) October 21, 2015 – December 31, 2015

In the charts above I have charted the 12 month performance of the broad based U.S. stock indices (chart #1).

Also above (in Chart #2), I have charted October 21, 2015 through December 31, 2015, because usually, October 21st through February 19th of the next year is a great time for equity investors. Normally, we see seasonal strength in the stock indices between October 21st and February 19th of the following year. I’ve done research on this and have determined it’s usually because of and due to increases in consumer spending (primarily holiday and travel expenditures), seasonally strong 4th quarter EPS of all the components of the broad based indices, mutual fund window dressing, the Santa Claus Rally, the January Effect, Congress being out of session, new government spending proposals, abatement of tax loss selling, and 401k and IRA contributions, etc. There are many reasons for the markets to do well at year end, and into the new year. This year’s year-end-rally hasn’t been that great, so far (except for Biotech, see ticker IBB, from October 21st through December 31, 2015) Click here for ticker IBB’s main components. Now, it’s never over until the fat lady sings! And it’s not February 19th of 2016 yet. But so far, performance hasn’t been that great. Regardless, I’m bullish going forward, full steam ahead. I firmly believe that if there is no recession looming, then there will be no bear market. And I firmly believe that there will be no materialization of any recession in 2016, or even early 2017.

2015 also saw some fantastic “blow ups,” including tickers FXCM, MNK, CMG, and VRX (click here for quotes on these). Bottom fishers might want to speculate in these, with high risk funds. Click here, for list of potential bottom fishing candidates; Know that it can always “get worse” before it “gets better!”

Within the energy sector are also many many stocks that have absolutely stunningly declined substantially off their mid 2014 highs. There’s plenty to choose from if you dig around a little, which could satisfy the bottom fisher’s quest for the rebound.

Also, BitCoin (click here for the wiki article), was listed in 2015 somehow as a commodity! GBTC is managed by a company called Grayscale, a Digital Currency Group Company.Click here for the commodity wiki article. I like to say the so-called BitCoin crypto-currency (whatever that means!) is like the board game Monopoly, and its Monopoly Money (backed by absolutely nothing!!! HA!!!). I suppose even Monopoly money is worth something, like maybe the paper its printed on. This BitCoin BS is the ultimate BS hype bubble right now, and it’s inflating very very rapidly! See ticker GBTC, it should prove to be highly amusing. Speculative asset bubbles are fun while they’re inflating, but they’re no fun at all when they go pop for those speculating in them!So, BE CAREFUL if you play with fire! I like to say it’s currently appreciating due to the greater fool theory, or kinda like hot potato. Bubbles to me are also like musical chairs, and at some point the music will end, and the bubble speculators will be left without at place to sit. Click here for the wiki article on bubbles.

I believe Monopoly Money is very similar to BitCoin.

Bubbles can inflate rapidly, but they can also pop, and suddenly burst; Stunningly devastating losses can mount up and materialize. Investors might be better off investing in literally trash versus BitCoin (ticker GBTC). Try what I describe as “The Four Kings of Trash,” Waste Management, Waste Connections, Republic Services, and Covanta, tickers WM, WCN, RSG, and CVA.

This BitCoin (ticker GBTC) mania and euphoria reminds me when the ETF ticker GLD first became listed on the exchanges.GLD (in my opinion) attracted so much money out of the securities markets (after it was listed as an ETF for securities investors for the first time) that it created a bubble in gold, which inflated, over the course of seven years, by roughly +311% gain (from 45 to 185), before popping and imploding. Today, I believe GLD is still in the process of popping (in my view), and has come back down to 101.46, as of 12-31-2015 (from the roughly 185 peak in July of 2007). I do not think gold (or the ETF ticker GLD) will see its prior peak for a very very long time.

I think commodities shouldn’t be listed on the securities exchanges. To me, commodities are not securities, and so they should not be listed on the AMEX, Nasdaq, NYSE, etc. for investors to trade like stocks. To me, commodities, belong at the NYMEX or Chicago Mercantile Exchange, and should solely be traded by commodities traders, in commodities accounts. I’m not sure why the CFTC, SEC, or the IRS has allowed the subversion of many commodities to be listed as ETFs on the securities exchanges for securities investors. Speaking of commodities gone wild, it looks to me like coffee, ETF ticker JO, is finally “on the move,” and 2016 could be the year of coffee bean prices!

Wrapping things up, I wanted to leave you all with a quote list of my favourite high yield stocks, in no particular order; Click here for that list.

Lets all hope that the god (or really goddess) of securities and investing, and of wealth, fortune, and prosperity, Lakshmi, brings better times ahead for investors!

Here are three great reports to assess the state of the economy: (1) Click here for the FOMC’s statements and minutes and estimates; (2) click here for the most recent edition of The Economic Indicators; and (3) click here for JPM Asset Management’s “Guide to the Markets” publication and analysis.

Lastly, here’s the current assessment of the U.S. Economy and its markets by Deutsche Asset & Wealth Management [click here for their current report].

Happy Trading!,

Andrew G. Bernhardt

PS- Here’s a great resource on (1) how all iShares are doing, click here; Also (2) here’s how all SPDR ETFs are doing, click here.

Some are voicing concern over the Dow Jones Transportation index, which is -7.19% YTD, however, if you go back more than YTD, say 1, 2, 3, or 5 years on a chart of the Transports against the DJIA, the Transports are outperforming; So to me there’s not much to be concerned about regarding that divergence YTD of Transports vs. the DJIA.

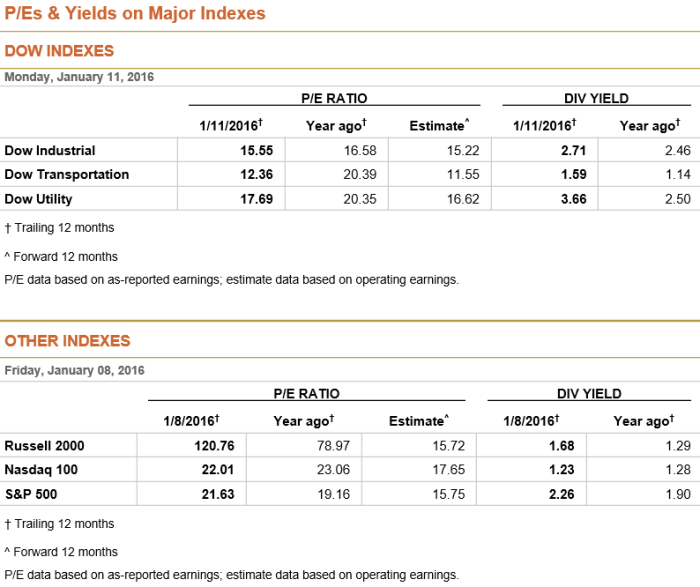

I’m currently rooting for the DJIA, matched by the ETF ticker DIA, as it has the lowest PE Multiple of all the Major U.S. Stock indices, and also the highest dividend yield relative to all other major U.S. Stock indices (with the exception of Utilities). The DJIA has also lagged the other major market indices YTD, and I think it will eventually catch up.I’d wait for a pullback before getting too aggressive with the indices here.I think the DJIA will close around 20,000 near year end, as Jeremy Siegel has speculated publically, even if we get a mini correction soon, or a full blown ten percent (or more) correction.

I’ve annualized the DJIA since about March of 1999 to the present, about 16.25 years ago (when it was at 10,000) it annualizes to +3.77%. This is well below the historical norms of roughly +7.50%. What has hindered the equity markets over the past 15 years or so has been the Roaring 90s, which set us up for the Tech Bubble of the year 2000 (the Nasdaq peaked at 5,132 on March 10, 2000- It still hasn’t reached break even with that figure from over fifteen years ago!), and what I describe as “The Greater Depression” of late 2007 to roughly early 2009. The S&P500’s performance over the past 16.25 years has been weaker than the DJIA due to its technology exposure (tech has been the biggest disappointment over the past 16.25 years… “Tech” is a four letter word!). The best equity performance over the long run can be found in the S&PMidCap400, which has had significantly more consistent and stronger earnings growth, and better annualized returns versus all other major U.S. market indices (see ETF ticker MDY).

In my view currently the VIX has gotten very very low, and should be indicating that you should be cautious going forward. Low VIX indicates euphoria and mania in the equity securities markets. There’s only been a handful of days where the VIX has been so low, for very long, and when it spikes, or increases, the equity markets can come tumbling down fast. This brings opportunity.

There’s an inverse correlation noteworthy of significance between the trajectory of the VIX, and the trajectory of every major stock market that there is, so when the VIX declines, the markets rise; and when the VIX ascends, the markets fall. I think since it’s so very low right now, it will likely increase, and the markets will decline.

My crystal ball tells me that we’re in for a mini-correction, of 3 to 5 percent before the markets will begin their ascent to new highs again. I’d remain cautious (holding cash) until we get a pull back in stock prices.

The main concerns going forward, are a low VIX; markets are at nearly all time highs; Greece is totally insolvent and may exit the Euro currency and the EU; and economic data has been weak in the USA and elsewhere; If and when Greece exits, investors will worry about Italy, Spain, and Portugal exiting the Euro currency and EU itself. Additionally, China is slowing (despite its recent booming stock market), Europe isn’t really that strong (and the European stock and fixed income markets may be in bubble territory, as is the case for the Euro currency itself); Russia is really hurting due to low oil prices; and Africa is fundamentally totally speculation (and is classified as a “frontier market;” There may be HUGE opportunities there in the future over the long run), and Central and South America are in a slump (Brazil has been very weak for many years now). Japan has also been weak, despite its stock market ascending. This tells me the backdrop for the economy worldwide is not really improving that greatly. PE Multiples are neither low, nor high, but they’re definitely closer to high, than low. Fear and market psychology over Greece’s insolvency could push the equity markets lower worldwide over the coming days and weeks.

Here (above) are the up and coming Greek Debt Payments… Many are expecting ultimately a default, which could bring about market turmoil.

Above is the Greek IMF required payments; Many are expecting a default, which would not bode well for the equities markets, or the fixed income markets worldwide. There definitely could be some turmoil over Greece’s conduct and behavior going forward.

I’d wait for a pullback (holding big cash positions) before getting fully invested and/or leveraged in equities, and more aggressive with the equities markets.I think bonds are in for more dire straights, and interest rates are going to rise in my opinion going forward; Rates were at totally unprecedented lows recently. How rates ever got that low, and stayed that low for so long, is beyond me! I can’t believe anyone would lend money to the U.S. Treasury at e.g. 2.33% for 30 year bonds a few weeks ago!!! Those rates were obscene, and were totally irrational! Fixed income investors will be treading water for quite some time in my view. Those invested at the long end are in for some more trouble I think. I believe that Treasury Security investors will be SHOCKED as to how much they can lose in e.g. 30 year Treasuries, as the duration and interest rate risk is very high (see tickers TLT and ZROZ, both of which are well off their 52 week highs!). Surprisingly, junk bonds and the high yield markets are nicely priced right now, I’m expecting more of a selloff to continue in Government bonds worldwide than junk and high yield bonds. You can see evidence of this in tickers: ZROZ, TLT, TIP, EMB, PCY, HYG, JNK, QLTC, etc.

Know historically the stock markets are weak in the months of February, May, and September, according to Barron’s Magazine (I would dispute and research February allegedly being historically weak, but I’ll just report what Barron’s has said recently).

I believe there will be fear mongers warning of a recession looming, due to the weak retail sales, weak producer price index, weak industrial production, an weak consumer sentiment; Not to mention the turmoil in Greece. I still think that after we get a mini correction the economy, in the USA and worldwide, will improve, bringing equity prices up (after a potential mini correction or full blown summer correction). There may have been a weak spot in the economic data due to a rather harsh winter season and very bitterly cold temperatures, which held back and discouraged the consumer (the biggest part of the economy) during the first quarter.

I believe there is increased risk of the first rate hike by the FOMC rate hike in 2016 by Yellen, not in September or December of 2015. Of course, there will be journalists saying and wondering if she’ll raise rates in June 2015. I believe she’s nearly spelled it out, repeatedly, that the FOMC will not raise rates in June, and at the earliest they might raise rates in September. Once we get closer to 2016, gurus will say and wonder if she’ll raise rates during an election year. I believe interest rates, at the short end, are going to remain low for quite some time (while rates at the long end will increase).

There are many who say higher rates will harm REITs (see the ETF ICF), and that it should benefit financials such as those found in the ETF XLF, and regional financials such as those found in the ETF tickers KRE and KBE.

I believe eventually the paranoia over higher rates will subside. The end of the world is not coming due to higher interest rates at the short end, or even at the long end. I do not believe the U.S. will have another recession until about late 2017 or 2018 (at the earliest), and for that reason I think the equity markets will continue to grind higher (after we get through some short term volatility and turmoil). I’m expecting a slight pullback and mini correction, followed by rebounds and a slow grind to higher stock prices for the next year or two.

Just because the market has risen sharply since March of 2009, does not mean it can not continue to increase. After all the annualized performance of the major U.S. Stock Indices since 1999 or 2000 (of roughly zero to roughly plus three-point-seven-seven) has not been anywhere near the longer term historical averages, of approximately plus seven and a half percent per year.