Tuesday, January 12, 2016 (3:30amCT)

DEEP THOUGHTS ON THE SECURITIES MARKETS AND THE ECONOMY

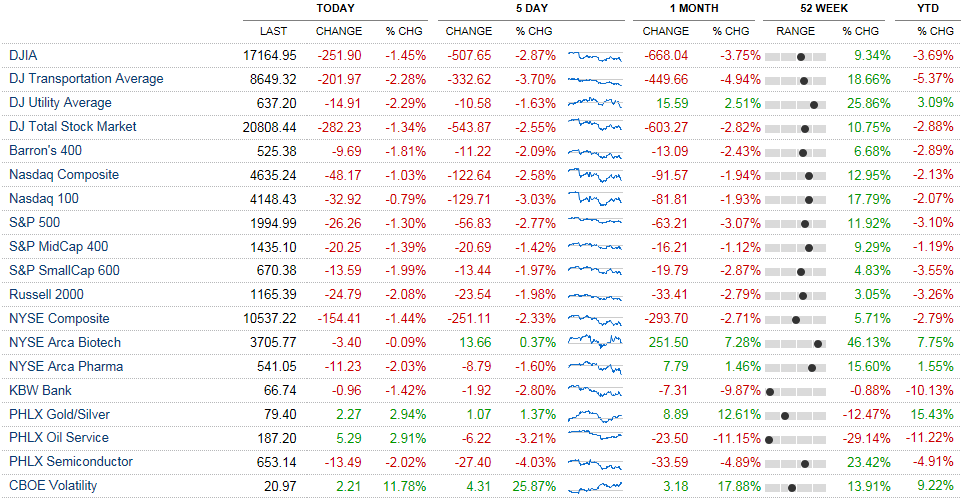

It’s been the worst start for a year… Ever.

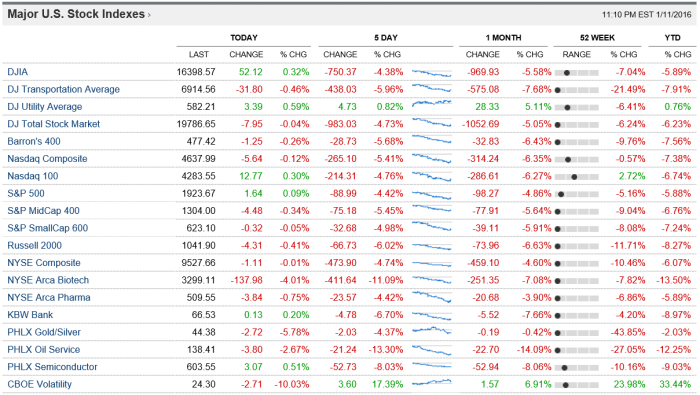

Do you know what I think of the most recent stock market sell off? I think it’s phony as hell! There is literally no catalyst I can think of that sparked the most recent sell off. So, in my mind, there could easily be a strong snap back rally, like in late August and September, etc.

When I think about “crisis watch,” “crises watch,” or “bubble(s) watch,” a game I play with myself and with the old wise men I know and trust, I (and we) can’t think of any valid issue looming to spark further selling. In my mind, the recent sell off has been completely and utterly irrational and illogical. Know that it can “get worse,” before it “gets better.”

Why are the indices 10 to 15 percent off their peaks? Why does everyone literally sell everything indiscriminately on low and lower oil?! Low and lower oil is great for the U.S. economy (it’s only “bad” for OPEC nations, and bad for the energy sector). It’s bad for Brazil, Russia, Saudi Arabia, Iran, Iraq, and Kuwait. In the USA the entire energy sector is allocated into the broad based indices around 2.59 percent to 6.4 percent. So, the energy sector is really a tiny sector of the US economy, and is a tiny allocation to its broad based stock indices. Let the whole f-ing sector go bankrupt due to its own inept incompetence and ignorance of total overproduction!

When I see oil trading lower (nearly every day now), I think “great” and also “the market should be surging!!!” The USA isn’t Kuwait or Saudi Arabia, it’s not Brazil or Russia either. I worry investors believe it is! Why have the broad based indices correlated to the trajectory of oil over the last couple months?! Oil has been going down for 8 to 9 years now! It peaked above 145 per barrel. Low and lower oil and energy prices are great for the U.S. economy because it’s like a tax cut, and it stimulates consumer spending and consumer sentiment, which are major components and drivers of GDP growth. There is literally no recession looming in our immediate future for the USA, not in 2016, and likely not in 2017 either. GDP growth is expected to accelerate worldwide, except for China which claims recently it has decelerated to just +6.5 percent GDP growth expected for 2016. There is no looming housing market collapse, there is no massive layoffs around the corner, and unemployment is low, and the labor market is strengthening. Additionally, real estate in the USA is also strengthening; It and REITs will not be highly damaged by interest rates going from zero to 25 basis points, or even if rates reached 1.25 percent, or even 4 percent. Even 3.5 to 4.0 percent fed funds is “accommodative.” Inflation is under control, and is very low, which should be great for PE expansion. Maybe in the next year it will reach a CPI-U of +2.0% to +2.5%. Interest rates have finally begun to rise, off of zero, and stand at 0.25 percent. Janet Yellen at the Fed is expected to raise rates to 1.00 to 1.25 percent by early 2017.

There is no boogey man coming for the markets, instead the markets just might boogey woogie higher!

Alternatively, if the markets continue their downward trend, I’m not sure what everyone will blame the nasty bear market on, if one materializes? Did the economic cycle die of old age? Was it paralyzed by interest rates reaching perhaps 0.75% in the future? Was it King Dollar, and the emerging market currency depreciation? Maybe investors worldwide are worried about extensive U.S. tax reform? Perhaps, there is political risk? Would “The Donald” or “Hill & Bill” really be that bad for our futures?! Do you think anything they even claim they will do will be done? Either of them doing anything will be met with total resistance and nothing they want will happen; So, nothing will change. Know usually though, election years are great for investors, and just because the markets completely fell apart during the last election doesn’t mean it will this time! It was a total coincidence to me during the last election that the markets imploded. The markets implosion from late 2007 through early 2009 was directly associated with the housing market bubble, reckless lending (the “NINJA LOANS” – no income, no job, and no asset loans), and too many fools (with terrible credit quality) who owned homes, who couldn’t afford it- especially once the economy went from boom to bust. There is no parallels today, to that reckless past of ours. Banks nearly don’t do anything, except checking and savings accounts, they nearly never lend anymore, and they are and have been regulated the f-ing hell out of; So, there’s no bad loans to go bust. The future is bright.

Who cares about the “bubble” popping (in its final stages) in China in its stock market?! The Chinese markets are already down more than fifty percent! The Chinese markets have not appreciated now for many many years, they’ve really been rolled back. How many bubbles in emerging market stocks have there been in the past 15 to 25 years?! It’s not the first or the last time there’s an emerging market collapse. I’ve said for years, emerging market stocks are like lotto tickets! Furthermore, who really cares about North Korea’s nuclear weapons testing?! Every country has tested nuclear weapons. Nuclear weapons have been around since the end of WWII, and I’m sure every country that wants them, has them; Its been over 70 years since they were first invented and designed, and unfortunately they’re very cost effective and cheap. The USA blew them up running tests constantly in the ’40s, ’50s, and ’60s (probably up until the nuclear test ban treaty in the mid to late ’90s!), under water, at sea level, and above sea level, underground too, and also at very very high altitude (which disgustingly and mysteriously knocked out all radio transmission signals worldwide for several hours).

To me the fear mongering, war mongering, and terrorism discount on the markets has been overdone. The pessimism, the fear, and paranoia over nothing has been overdone. Volatility is very elevated to me.

At some point sanity will return.

The only risk I see lately, is that the perception is that higher rates will increase the value of the U.S. dollar against the euro, and also especially against emerging market currencies, reducing our exports, leading to a drag on sales volumes, and also on foreign earned income. The ruble has been particularly weak, china has been artificially depreciating its currency the yuan aka the renminbi. Brazil is having its worst recession in at least 30 years, thanks to low and lower oil, and rapidly depreciating commodities like coffee, and sugar, etc. Brazil is also plagued by low prices for iron, juices, cars, petroleum, tobacco, soy beans, poultry, and meat. At some point, Brazil is going to be a fantastic opportunity for investors. It like Russia, will likely reach rock bottom, once oil hits rock bottom.

When will oil hit rock bottom?! It’s anyone’s best guess, but I think we’re getting close, and it’s likely at some point in the next 2 to 4 months. Oil can’t decline substantially every day, forever. Oil, energy, and basic materials will likely represent a huge opportunity for investors as well, once oil hits rock bottom.

I believe the future is bright, and despite the worst start for any year, I still believe that the U.S. broad based stock indices (matched by tickers: VTI, DIA, SPY, MDY, and maybe IWM) represent the best investments for long term (10+ years) investors. I also really like tickers EMB and PCY (which match the U.S. dollar denominated JPM EMBI), and over the long run, over every 24 months or greater, I believe that these tickers will provide positive total returns.

I think it’s time to be bullish. There’s a small chance of total idiocy and paranoia and a huge market sell off, to a depth of maybe -30 to -40 percent off the all time highs of the broad based stock indices, but with no valid or logical or rational catalyst, I really don’t see that happening, until there is actually a recession. I firmly believe that there is no recession looming (anytime soon) in the USA (not in ’16 or ’17), so I see no reason for a bear market materializing.

Here are some reports to use, to assess the economy of the USA and the world.

(1) Minutes (releases, statements, accessible materials, implementation note, and projections; and press conference) of the FOMC;

(2) The Economic Indicators [November 2015];

(3) JPM Asset Management Guide to the Markets.

Happy trading,

Andrew G. Bernhardt