Sunday, March 29, 2015

My Thoughts & Market Update

The Major U.S. Stock Indices declined the week of March 23rd through the 27th, see the graphic below for their 1 day, 5 day, 1 month, 52 week, and YTD performance.

Market Performance (through Friday, March 27th, 2015)

As you can see the DJIA, the DJ Transports, and the DJ Utilities are now down YTD. I remain bullish, as I believe the economy may have had a recent soft patch due to the extreme winter weather and blizzard in the north east as of late. I believe the economy will make a comeback and the markets could appreciate going forward from there. Jeremy Siegel believes the DJIA could reach 20,000 by yearend. (Click here for that video & article). If we get to 20,000 by December 31, 2015, that would be a +12.9136% move, from Friday’s close of 17,712.66. The labor market continues to improve, and inflation remains very very low; According to many economists, lower energy and fuel prices should also bolster and assist economic growth; Know that in 2007 through 2009 lower oil and energy prices really didn’t bode well for the economy worldwide (there have been reduced payrolls and reduced capital spending in the energy space, and energy company stocks comprise about 10 percent of the S&P500 and lower oil prices do not bode well for these companies or for their earnings, nor does a very strong dollar… a strong dollar can lead to wider trade deficits, less exports, more imports, and diminished earnings brought home from large multinational corporations. Peter Lynch always said “earnings drive the market.”). Click here for the highlights of the BEA’s Economy at a Glance. Yellen (I believe) will have to have the CPI actually increase (by the average +0.20% per month for a few months in a row) before she can justify perhaps raising interest rates; I continue to believe that rates could remain close to zero through June, possibly through September, and into 2016 due to low inflation, and the weakest economic recovery on record, post any recession. Additionally, China, Japan, and Europe appear to be weakening, which may pressure the Federal Reserve to keep rates low.

Lately, Yellen has also voiced some concern over demographics, and lack of population growth, and economic growth going forward (see this article). As we all know (or as we all may know), the birth rate, the fertility rate, and the age of first marriage have really changed since the ’60s with the advent of birth control. Basically, women are having few children, and they’re having fewer children later in life (women’s labor force participation rates have changed, family units have become more broken over time, and the age of first marriage has also increased greatly, all since, on average, 1960). This is straining Social Security, as the direct transfer from the working to the retired doesn’t work very well, if there are fewer and fewer children, because these children who never are born or had (due to birth control pills), don’t grow up, and they don’t find themselves in the labor force working, to make e.g. Social Security and all the generous entitle programs more solvent; on the contrary they become less solvent with less and less children and lower birth rates and lower fertility rates. This could be a major headwind for 1st world countries going forward well into the future, in the coming decades (Japan and Europe have major problems as well with this, as birth control pills have become even more popular over there relative to the U.S.). These concerns could be used as an excuse to keep rates very very low by historical standards. Maybe some day, creditors will be rewarded? Know that you can buy fixed income on margin (Reg T allows for initial margin maintenance requirements of less than 50% for Treasuries, Agencies, and Municipals), and there are low margin interest rate brokerages, such as Interactive Brokers (and others) who is rated very highly by Barron’s Magazine. Click here for The Board of Governors, Federal Reserve System, FOMC’s website, of Economic Forecasts, transcripts of Minutes, and their video news conference (of March 18th, 2015).

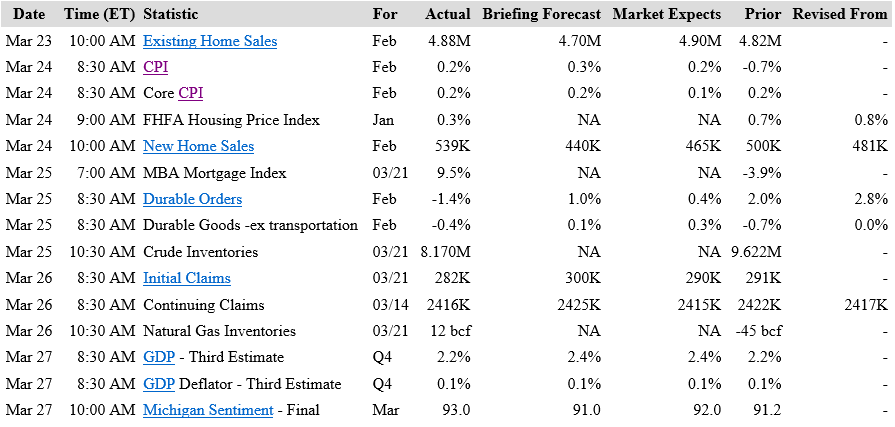

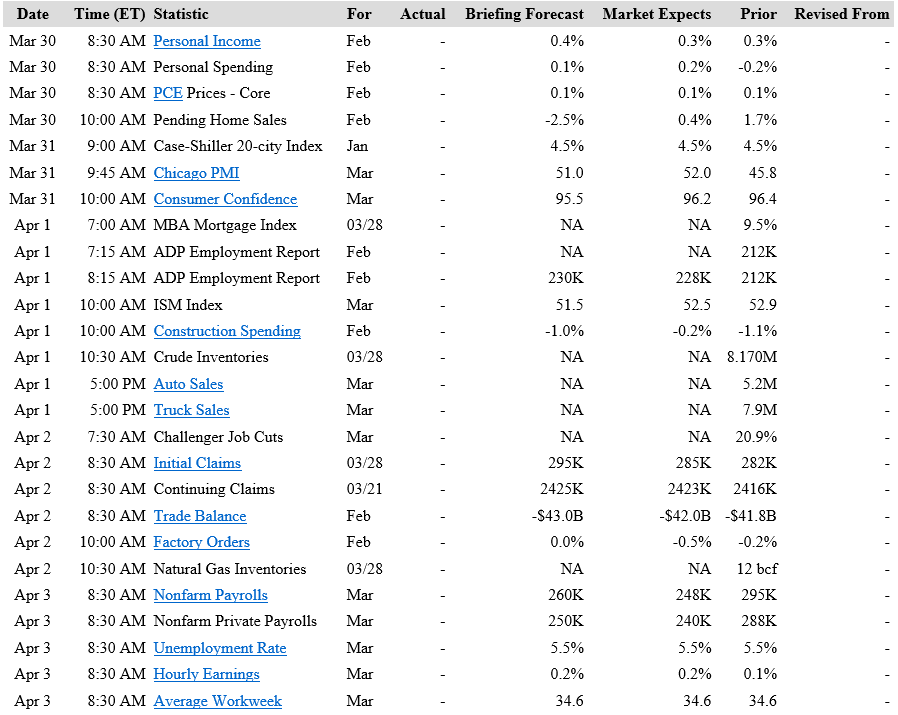

Below is the economic calendars for this past week, and for next week.

Economic Calendar Last Week (above)

Economic Calendar This Week (above)

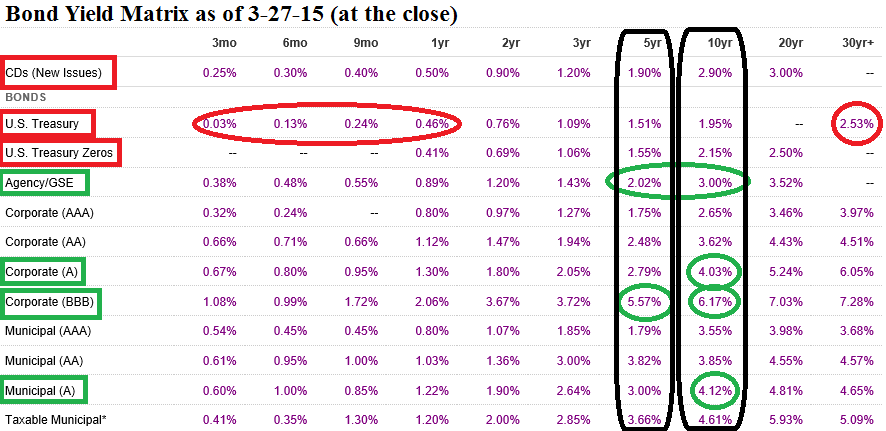

Below is a bond yield matrix, of current yields by issuer, credit quality, and maturity. I have circled in red what I think should be avoided, and I have circled in green, and have put in a black rectangle, what I think looks good, in my view. I believe ten years is as far away in terms of maturity that anyone should speculate with. Also, click here for Bill Gross’s Fixed Income Investment Commentary. Last month Bill Gross (who is widely believed to be “The King of Bonds”) discussed the board game Monopoly, this month he talks about pets and dogs.

Bond Yields by Issuer, and average credit quality, and maturity, through Friday, March 27, 2015.

Kiplinger’s March Economic Outlooks (above)

Notice how Kiplinger believes oil will be trading significantly higher. I think ticker USO (which matches the performance of West Texas Intermediate crude oil) is beginning to look appealing, as is XLE (the energy sector etf), and some individual energy and oil company stocks… such as tickers XOM, BP, BPT, CVX, and COP. These could prove to be great long term holds, for patient investors, some of these securities sport high dividend yields.

Select Quotes of Interest (Friday, March 27, 2015)

[CLICK HERE for an update on the above quotes]

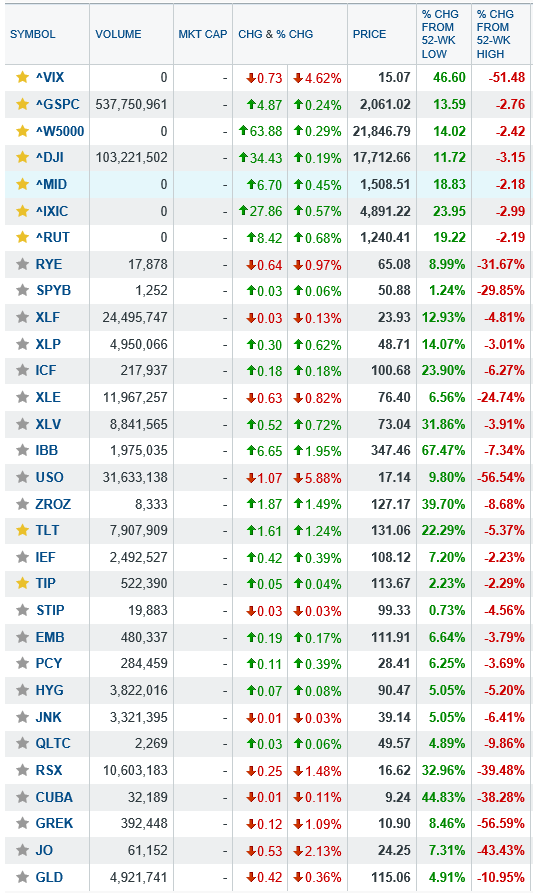

Notice how most of the Major U.S. Indices are now 2 to 3 percent off their all time highs. Perhaps it’s a good time to get invested (indexing based investments over the long run are a great idea, see tickers VTI, DIA, SPY, MDY, IWM, ICF, and QQQ). Buying on dips can prove to be a great idea, over the long run. Notice how USO (which matches the performance of West Texas Intermediate Crude Oil) is now 56 percent off its 12 month highs, and XLE the energy sector etf is 24 percent off its 12 month high. I’m bearish on the etf IBB as I believe the hype surrounding biotech is and has gotten extreme; Some major components of IBB have doubled in stock price in the past three months and have triple digit pe multiples! Some of these companies think they’ll cure cancer! I’m also bearish on the long end of the yield curve, so ZROZ and TLT are, I believe, going to continue their downward slide, as they have extreme interest rate risk, as measured by duration, and I believe interest rates will increase all along the entire yield curve, in my view (which will most harm bonds at the long end). Surprisingly, junk bond spreads are quite normalized, and junk bond current yields are not at unprecedented (or nearly unprecedented) low yields as Government, and AAA, fixed income yields are. I believe there are opportunities to be had in BBB and BB rated “junk” aka high yield fixed income; See tickers EMB (EMB is my favourite- and The J.P. Morgan Emerging Market Bond Index (“The EMBI”) has also been a long term favourite of the Harvard and Yale Endowment funds, as well as a favourite among many Pension funds). Also see tickers PCY, JNK, HYG, and perhaps even QLTC (these are all in the junk bond and high yield space); Ticker SJNK is a short term maturity junk bond etf also, and may well prove to be a great long term investment as well (talk with your advisor, there’s tons of opportunities to be had, and CONSTANTLY!). I believe the 30 year Treasury bond has perhaps had a sea change, and that we’ll potentially never again see the low yields reached (and high bond prices reached) of January 29th, 2015. I believe rates could move significantly higher over the years from here. I believe the bond market rally (at the long end of maturities) of roughly 1982 to January 29th 2015, is over! I believe that investors will be shocked at just how much can be lost in 30 year Treasuries (and 30 year Treasury Zero Coupon securities) over the next 15 years. In 15 to 20 years, investors may be able to purchase Treasury bonds issued in January and February of 2015 at MAJOR DISCOUNTS. Beware of duration of your fixed income portfolio, the interest rate risk might be at extremes at this time. Lower durations and maturities of ten years or less have significantly less interest rate risk versus their 30 year fixed income counterparts.

PE Multiples of the Major U.S. Stock Indices (as of Friday, March 27, 2015)

Notice how the DJIA has a PE Multiple of just 16.63, that’s cheap to me, and I believe it can only mean (or suggest) it may move higher this year; Additionally, the dividend yield of the DJIA has increased in the last 12 months from 2.43 to 2.51 percent for the DJIA, which I believe is a bullish indicator.

Headwinds for the stock market continue to be the following: increased violence (and the waging of war) in the Middle East, Russia’s “Sabre Rattling,” and the default risk of (Russia) and Greece. Additionally, I can’t see how negative interest rates in Europe can be good for that region of the world. I’m not sure how or why or how their stock markets are up roughly 10% this year (as measured by tickers EFA and IEV, and EWG, et al). Know that the economies of Japan and China are also slowing down.

Click here for a copy of the most recent CPI-U Data Release; and click here for the most recent GDP Release.

Happy Trading!

Andrew G. Bernhardt

[Click here for my Great & Useful Links Page]

[Click here for all the tickers I like to follow daily]

[Click here for Futures vs. Fair Value, to see the Implied Open]

[Click here for Yellen’s Worries on Low Population Growth] – Which I say is because of birth control pills; This could lead to $85 Trillion dollar Federal Government deficits in the USA in the future (see Kotlicoff’s “The Coming Generational Storm”). Who would you blame for this (the birth control pill issues, and enormous deficit projections in Europe and the United States)?? Would you blame the incompetent lawyers and the ABA, or the incompetent medical doctors and the AMA who prescribe the birth control pills?! Why are these pills legal with such nasty economic consequences? Feel free to leave comments below.