On the Securities Action of Monday, February 2, 2015

STOCKS RALLY ON WALL STREET! Monday saw a broad based rally across the board on Wall Street. Volatility, as measured by the VIX imploded and was -7.34% to 19.42. The S&P500 finished up + 1.30% or 25.86 points to 2,020.85, the DJIA was up 1.14% or 196.09 points to 17,361.04 In fixed income, Treasuries were down while high yield sovereigns and corporate debt rallied. I’m remain bullish and believe stock prices will go higher, lead by the energy sector, as I believe oil will trade higher from here.

Feb. 2, 2015, Major U.S. Stock Indices

The DJIA is now -4.10% off its peak reached at some point in the past 12 months, the S&P500 is -3.47% of its peak, the S&PMidCap400 is -2.10% off its peak, the Nasdaq Composite is -2.87% off its peak, and the Russell 2000 is now -3.76% of its peak, the Wilshire 5000 is now -3.15% off its peak. XLF, an etf basket of financials, was up +1.61% to 23.38, and now stands -7.00% off its peak reached in the past 12 months. XLE as basket of energy shares, was up +3.06% to 77.87. XLV, a basket of pharmaceuticals was up +0.56% to 69.66. ICF a basket of REITs was up -0.03% to 103.80. Crude oil traded up strongly, for the second trading day in a row, USO an etf of West Texas Intermediate, traded higher by +4.49% to 18.62. USO stands down -52.79% off its peak reached at some point in the past 12 months, I believe in late June. I believe oil will remain volatile, but I think that it has bottomed, and that higher prices of oil will drive energy sector shares higher, which will lead the market higher.

Quotes of Interest

[http://finance.yahoo.com/futures] Click here for an energy prices update.

In the Fixed income markets, ZROZ traded lower, down -0.24% to 138.65, TLT traded down by -0.38%, IEF traded lower by -0.12% to 110.23, TIP was down -0.07% to 115.55. EMB was up +0.10% to 111.49, PCY was up +0.38% to 28.89, HYG was up +0.39% to 90.21, JNK was up +0.23% to 38.84, and QLTC traded higher by +1.78% to 49.18. The 30 year Treasury yield settled at 2.25%, the 10 year Treasury yield settled at 1.68% [data from here: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield]. I continue to believe, and will reiterate, that if oil can stabilize in a trading range, or start to appreciate, that there will be some major opportunities in the energy sector in equities, and in their high yield fixed income; Also I continue to believe that when oil stabilizes (or begins to appreciate) that there will be some major opportunities in high yield fixed income funds, such as the ones listed above, EMB, PCY, HYG, JNK, and QLTC.

The US Dollar traded slightly lower versus the Euro on Monday, the Euro gained approximately +0.32%, as measured by the etf FXE. I continue to believe the Ruble and the Euro are still too high, and will further deteriorate, making the dollar stronger. The U.S. Dollar can now be exchanged for a Euro at a cost of approximately $1.1335, and also can now be exchanged for 68.0945 Rubles.

[http://finance.yahoo.com/currency-investing] Go here for an update on all major cross rates

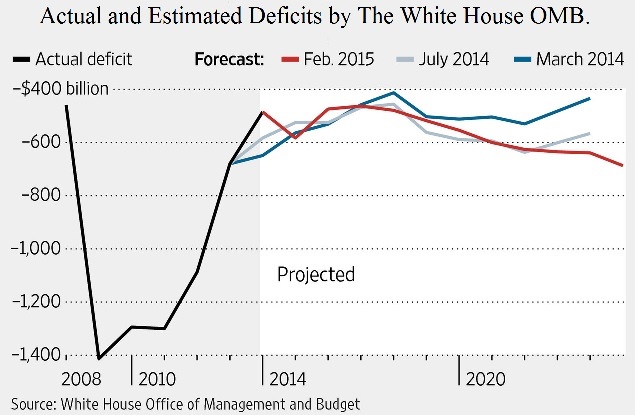

I believe the catalysts for today’s stock market gains were predominately higher oil, the release of the Federal Budget by the Obama Administration. The Budget proposal calls for an increase in defense spending of +4.50% from last year, and in sum is $3.99 trillion of expenditures, (+6.4% increase from last year) and with an estimated revenue stream of $3.53 trillion; The estimated deficit is projected to then be $474 billion dollars. Government economists are estimating and projecting that deficits will be 2.5 to 3.5 percent of GDP annually for the next 10 years.

What we need is a President and Congress who will actually try to balance the budget and/or try to run a surplus. The Executive and Legislative branches of Government shouldn’t crowd out investment and crowd out borrowing until there’s a panic in the markets and a recession; They borrow like there’s no tomorrow. They are siphoning money away (by borrowing billions per day!) from other causes with their deficit spending. We also need a Legislative Branch that doesn’t e.g. reduce regulations mortgage lending standards, to literally let anyone buy a home, as they did in 2000 through 2008. This I believe set the USA up for a real estate downtrend which began in roughly 2003 or 2004, which ultimately took the rest of the economy downwards with it starting in late 2007 through 2009. They shouldn’t have been able to buy these homes in the first place. We also don’t need a Congress so foolish that it thinks it can punish financials (banks, brokerages, insurance, and reinsurance companies) with hefty fines, penalties, and indictments, from Federal Prosecutors at the DOJ, who crazily believe that their “crack down” on these financials will stop the economic cycle and prevent future recessions. It was their idiocy of excessive borrowing, and changing of rules to let fools buy homes in the first place that caused the economic troubles of the late 2007 through 2009. Their new regulations will do nothing but cause more trouble. Increased lending standards that literally prevent spending (by limiting credit and limiting loans) is ridiculous. Ben Bernanke couldn’t even refinance his home recently! We need a “do nothing” Congress. Lastly, I believe that Elizabeth Warren’s protections of the consumer are ultimately damaging these same consumers, by harming their investments. We don’t need a Consumer Protection Financial Bureau, we need a Corporate Protection Financial Bureau. What does Elizabeth Warren want ultimately? Zero percent profit margins?! Should all companies have to reorganize into a 501(c)-3 Corp?! The Congress and its members needs to think at a higher level (or at least try). This could perhaps start with higher standards for the LSAT (the law school admissions test) and for law schools in general, since most of our Congress is filled with lawyers. It begins with education and higher standards.

Also with the President’s budget release, I believe Obama is suggesting that he’d like to bring back foreign earnings of multinational corporations held offshore, by suggesting a new tax levied of 14% on those accumulated earnings and 19% on recently earned profits abroad, in an effort to have those earnings brought back to the USA. The OMB projects and estimates that interest payments on our national debt (to debt currently at $18 trillion and 82 billion dollars) will be 13.5% of expenditures in 2025, up from just 6.5% today. For “The Debt to the Penny,” (the total U.S. Federal Government Debt Outstanding) click here: http://www.treasurydirect.gov/NP/debt/current. The $18 trillion of Federal Government debt doesn’t include State, County, Municipal or Local Debt, nor does it include private sector debt, or corporate, or agency debt. Americans sure like borrow and spend! There are few corporations on the S&P500 with zero debt. Click here for an article and listing of 26 companies with zero debt (as of May 29, 2014): http://americasmarkets.usatoday.com/2014/05/29/debt-free-26-u-s-companies-shun-debt/

Click this link for a White House OMB website with many links on the Obama Budget: http://www.whitehouse.gov/omb/budget/Overview. Click this link for a White House OMB release website with the entire Federal Budget (it’s 150 pages long, and is a PDF of 2.3 mb in size): http://www.whitehouse.gov/sites/default/files/omb/budget/fy2016/assets/budget.pdf

Economic data releases on Monday were weak across the board, I believe fueling traders’ expectations that higher rates will be delayed by the FOMC. Also next week newsworthy reports will be Monday’s Personal Income and Outlays came in as expected at +0.30%, Personal Spending was weaker than expected at -0.30% (expectations were for -0.20%), Core PCE Prices came in as expected at 0.00%, ISM was slightly weaker than expected (at 53.5, while expectations were for between 54.7 and 55.0), and Construction Spending came in at +0.4% while economists were expecting +0.8% to +0.9%.

In notable eps reports due I think CMG will be amusing, as will WYNN, both eps are reports due after the market close on Tuesday the 3rd. I believe that CMG may move by ±51.00 on Wednesday the day after it reports eps. Yes, really fifty-one dollars of an increase or decrease in per share prices for CMG for Wednesday. So fasten your seat belts! We’re about to find out how many burritos were sold at CMG! I believe that a long bull call ratio back spread with net credit characteristics may be lucrative; Especially if also combined with a long bear put ratio back spread with net credit characteristics on CMG, placed tomorrow just a minute or two before the close (3:00PM Central Time). WYNN could perhaps move by ±7.70. It will be amusing to see what happens. Happy earnings speculation!

In other news, BP reported its quarterly eps, which beat expectations, but were lower than year ago (during the same quarter); BP reported $-969 million in earnings versus $1.51 billion a year ago. BP traded higher Monday, up +2.65% to 39.86. Looks to me like shares of BP reached rock bottom around January 12, 2015. XOM traded higher as well, and Monday was up +2.47% to 89.58; CVX was higher Monday as well, +3.44% to 106.06. XOM and CVX look to me like they may have bottomed on the 29th and 30th of this month.

I remain bullish, and believe that higher oil prices may lead the energy sector higher, which I believe will lift all major U.S. stock indices.

Some energy sector stocks currently have very high dividend yields (which I’d caution could or may be cut, but then again, they may not be cut). Checkout the yields on XOM yielding 3.20%, CVX yields 4.20%, BP yields 6.20, BPT yields 13.80%, and RIG currently yields 18.40%. I believe that if oil has stabilized these stocks also have some room for major price appreciation of the shares over the long run (within a couple years). Lastly, the etf XLE (a basket of energy related large caps) is currently -23.31% off its peak reached in late June of 2014 (101 and change was its peak, and closed Monday at 77.86). XLE could be a winner going forward for traders and investors who are patient for a few years. Happy trading.

Below are some more fun charts of economic data.

By Andrew G. Bernhardt