Monday, October 2, 2017

(Before market open)

End of the 3rd Quarter

Market Checkup

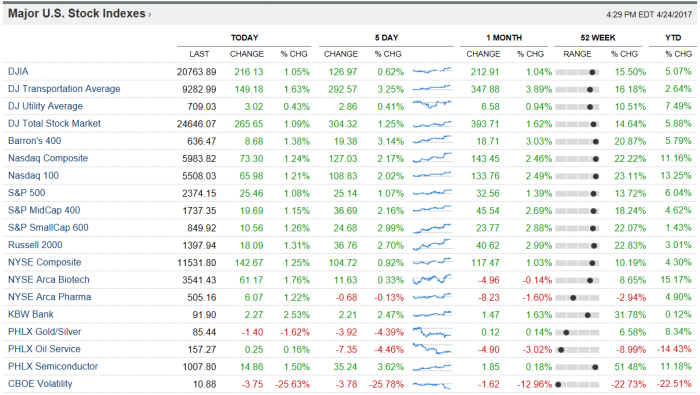

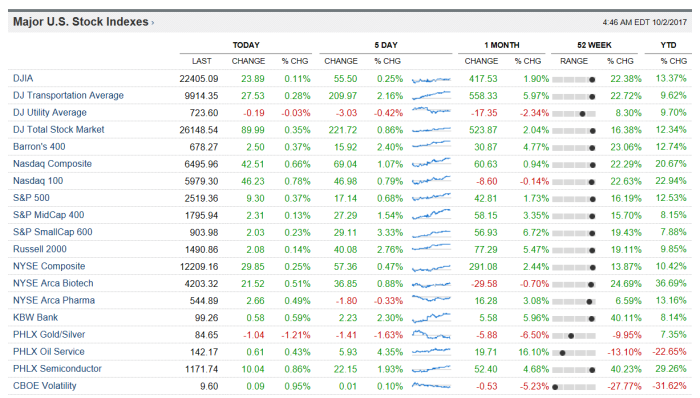

It’s the end of the 3rd Quarter and the year 2017 so far has flown by fast! Despite many risks, the broad based U.S. stock indices have increased nicely. [According to the WSJ’s statistics above] The DJIA +13.37% YTD (matched by ticker DIA), the DJ Transports +9.62% YTD (matched by ticker IYT), The S&P500 +12.53% YTD (matched by ticker SPY), the S&PMidCap400 +8.15% YTD (matched by ticker IJH), the Russell2000 +9.85% YTD (matched by ticker IWM). Tech (despite being a four letter word) has increased by +22.94% YTD as measured by the Nasdaq100 (matched by ticker QQQ). Additionally, the DJ Aerospace & Defense Index has risen by +27.57% (matched by ticker ITA). In the fixed income arena, the JPM EMBI (matched by ticker EMB), a fixed income index of sovereign high yield has (according to the EMB website) increased by +8.78% YTD. U.S. Corporate high yield junk bills as matched by ticker SHYG is +5.16% YTD (according to the SHYG website).

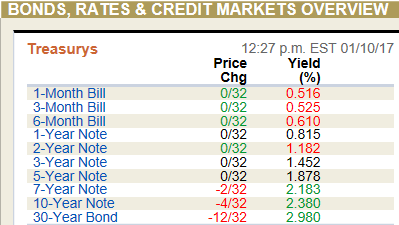

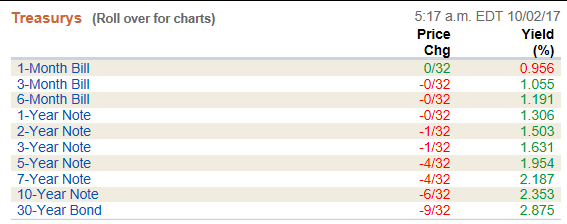

Treasury rates (see above image) are still, as I like to say, “supid low.” Who would lend money to anyone (including to the U.S. Government) at these rates?! To me anyone that buys Treasury Securities is ripping themselves off; Then again rates are negative in Japan, Germany, Italy, Spain, and elsewhere, so any positive yield might look great to foreigners. The 3 month T-Bill yields 1.055%, and the 2 year Note yields +1.503%, and the 10 year Note yields 2.353%, and the 30 year Bond yields 2.875%. What a joke Treasury yields are! To me serious fixed income investors invest in the following tickers EMB, PCY, SHYG, and SJNK.

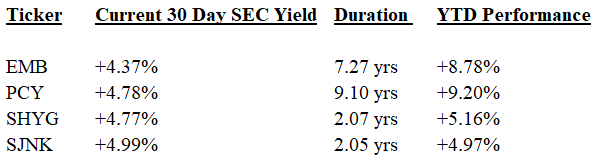

As you can see, the current 30 day SEC yield of EMB (which is sovereign high yield) is 4.37%, and the ETF has a duration of 7.27 years, and [according to the ETF’s website] is +8.78% YTD. PCY has a 30 day SEC yield of 4.78%, a duration of 9.10 years, and YTD is +9.20%. SHYG (which is U.S. corporate high yield junk fixed income) has a current 30 day SEC yield of 4.77%, a duration of 2.07 years, and YTD is +5.16%. SJNK has a current 30 day SEC yield of 4.99%, a duration of 2.05 years, and YTD is +4.97%. To me, SJNK seems most appealing (in fixed income) because the current 30 day SEC yield is +4.99% and yet the duration is also really low at 2.05 years.

Lets review some risks for investors going forward.

- Janet Yellen’s term at the Federal Reserve ends on February 3rd, 2018, and usually if any Chairman (or Chairwoman) steps down, there is a mini-scare and mini-panic, and a correction materializes in the stock markets, as anxiety creeps into the psyche of investors. Perhaps, they’re worried about getting a weirdo like Paul Volcker, who in July of 1981 raised short term interest rates to 14.00% (See a historical chart of the Fed Funds Rate Here). There is speculation that our current Treasury Secretary Steve Mnuchin will be nominated by President Trump to take Yellen’s place.

- Interest Rates are on the rise (see this chart) as set by the Federal Reserve. If they are perceived to get too aggressive with rate increases, a recession could materialize, bringing with it a pull-back, a correction, and a bear market for stock holders worldwide (including the USA). Beware of an overly aggressive Fed. Higher rates will also spell TROUBLE for fixed income, so reduce your durations to mitigate risk, if you trade fixed income (e.g. you don’t want to be in 30 year zero coupon Treasuries while rates rise). So, SHYG or SJNK looks better to me versus e.g. ZROZ or TLT. For maximum price stability (and for maximum reduction of risk) try tickers SHY (a 1 to 3 years to maturity Treasury Bill Index ETF) and IEF (a 7-10 year Treasury Note Index ETF).

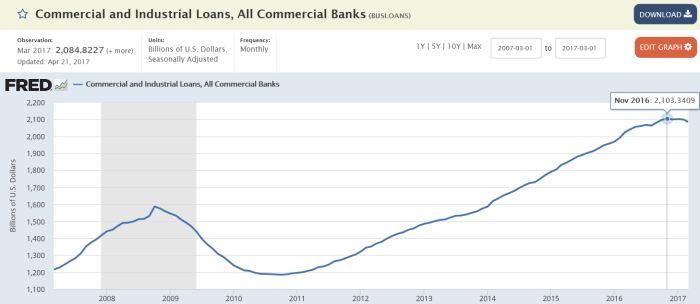

- Higher interest rates will also affect auto loans, home loans (and mortgages), housing prices, educational loans, credit card spending, and other spending habits of approximately 320 million people in the USA, and the remainder of 7.2 billion people on earth. Less borrowing and spending by Americans will turn into less income for everyone (watch total commercial & industrial loans in the data and on charts here).

- In addition to rising interest rates the Federal Reserve and the U.S. Treasury have decided to “wind down” TARP and sell their accumulated $4.5 trillion dollars of fixed income securities. This selling pressure of $4.5 trillion of fixed income securities will put upward pressure on interest rates across the entire yield curve. They say they’ll sell them off (“quietly in the background”) at approximately $10 billion dollars per month, escalating to $50 billion dollars per month. No one likes higher interest rates, as everyone (the U.S. Government included) appears to be a net borrower, not a net creditor or net lender.

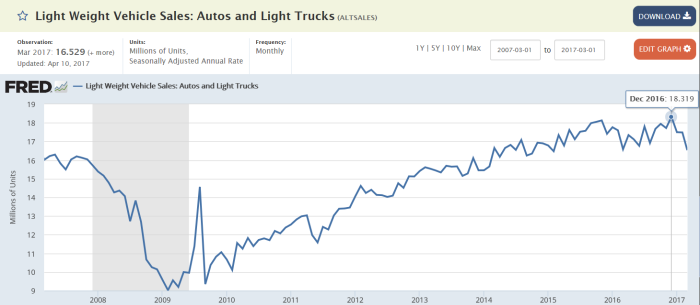

- The Hurricanes is likely to impact GDP and GDP Growth of the USA negatively (at first), while in 2018 the rebuild efforts which will materialize for Texas, Florida, Puerto Rico, and the U.S. Virgin Islands is likely to bolster GDP and GDP Growth. However the losses of economic activity in e.g. Corpus Christi, Miami, San Juan, Charlotte Amalie may not ever be replaced. The hurricanes which have devastated these cities will also likely impact our nation’s car sales figures positively, and could materialize into boons for Home Depot, Lowe’s, Ford, General Motors, and home builders (see ticker ITB), while being a negative drag to nearly everything else. The hurricanes will also likely increase (negatively) initial claims and also unemployment figures.

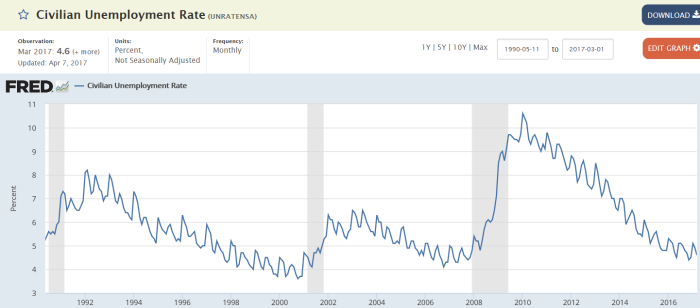

- Watch the hurricanes have impacts on the data & charts here: On GDP, Unemployment (beware of rising unemployment, which was already off its low- Further increases in unemployment could signal the end of the current economic boom cycle, this is very very serious), Total Vehicle Sales (vehicle sales were beginning to decline, but I have confidence that after these hurricanes, the figures could begin to improve again).

- There are also risks of “rocket man” (otherwise known as the leader of North Korea) and his obsession with terrorizing the world with his nuclear weapons testing, rocket testing, and other egregious actions with his military. Lately, he likes to fire ICBM tests over the land belonging to Japan, which is very worrisome, especially if there was some sort of malfunction during the test, resulting in the missile landing on Japanese soil, rather than out in the ocean somewhere. War mongering and fear mongering is a real risk, which has been fueling the Aerospace and Defense industry (e.g. ticker BA, Boeing, is up over sixty-three percent this year- See YTD data on the DJIA components here). Fear mongering and war mongering could also lead to higher oil prices, which could rise if a war breaks out anywhere worldwide (click here for a crude chart currently at $50.84; click here for a brent crude oil chart currently at $56.05). Then there’s always the possibility of further invasions of Iraq, Afghanistan, Syria, and elsewhere (for some reason Trump even mentioned the possibility of invading Venezuela, although I’m not sure if it would be for humanitarian purposes or otherwise).

- As previously mentioned, beware of unemployment rising, (and beware of declining labor force participation rates) as it could signal the end of the current economic boom cycle. It appears as though the unemployment rate struck rock bottom this April at 4.10%, and it has currently already crept up to 4.50% (through August). The current expansionary boom cycle started in March of 2009, and this cycle is nearly the oldest boom cycle on record for the USA (in other words the current boom cycle has been one of the longest lasting expansionary boom cycles). Once the party is over in the USA (since we’re a huge part of the world’s GDP), a pull back, correction, and bear market in stock indices worldwide will likely result; and a recession could materialize, which will likely discourage investors and demoralize people worldwide. So be careful. Once the stock indices are down by twenty-five to thirty percent, in a recession and bear market, you might want to consider increasing exposure to the stock indices, as rebounds generally rally through prior all time highs, and the rally could last years.

- The total Federal Government Debt Outstanding is over twenty trillion U.S. Dollars (see the Treasury’s website on the debt to the penny here), and is currently $20,203,668,853,807.76 (as reported 9-28-2017). When we will ever have a responsible President and Congress is anyone’s best guess. But the USA is not sustainable with trillion dollar deficits annually, or half a trillion dollar deficits annually. They need to control their spending and appropriations, and they need to put an effort into balancing the budget, and then in running a surplus. Otherwise, eventually, there could be a currency crisis, and a total default crisis in the USA, and a total economic collapse and catastrophe in the USA. Surely, the U.S. Congress will love to blame banks (and the whole financial sector of the economy), hedge fund managers, investors, and risk takers, but it is really them who are playing “Russian roulette” with our future and the economy. Borrowing excessively, crowds out borrowing, crowds out investment, and incites a credit crunch. Surely, the U.S. Congress will also pretend in the future, during the next crisis, that more regulations and more laws are the solution; But recessions can not be outlawed or prohibited. Their idiocy will surely be amusing and pathetic, it always is- So stay tuned! The irresponsible fools of our U.S. Congress (who I like to say are incompetent, illiterate, ignorant, and who can’t count) authorized the borrowing of literally $317,589,836,297.00 between literally just September 7th and September 8th of 2017. Yes, literally, over three-hundred-and-seventeen-billion-five-hundred-and-eighty-nine million dollars in just one 24 hour period. What clowns. Are they trying to incite a credit crunch and total default?! (Click here for data on the deficit or surplus of the USA). Recently, the Total Federal Government Debt Outstanding now exceeds the USA’s annual GDP (this is known as the Debt to GDP ratio).

- Many say that gridlock is bad in Washington, DC, but I’ve noticed that a “do nothing” Congress has been great for the economy and the markets over the past nine to ten months (and before in the past). Besides, when was the last time the Congress did anything that everyone liked. Gridlock is good. Didn’t Gideon J. Tucker say “no man’s life, liberty, or property are safe while the Legislature is in session.” So, will we get less regulation (or deregulation) of financials? Will the U.S. Congress get some tax reform through? We shall see.

- Consumer confidence, consumer spending, and consumer sentiment are at nearly all time highs. Can it really get any better from here, or is this as good as it gets, as I have written about in prior blog posts (click here for that).

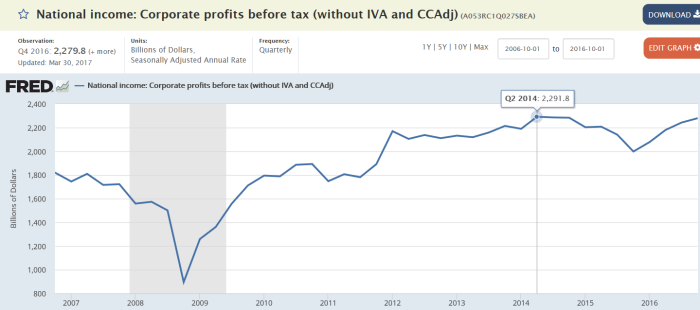

- Watch corporate profits before tax (click here), currently at 2,254.30 in Q2 of 2017, which have yet to eclipse the peak from Q4 of 2014 of 2,292.50. This is not a typo, corporate earnings are down, and yet the markets are up strongly since Q4 of 2014, eventually “something has got to give,” as they say. Going forward, we don’t want to see these figures stall out and begin a decline. Rising profits (and steady or improving labor force figures) will be required to take the stock indices to a higher level.

- The volatility index, the VIX is very very low right now at 9.53. A VIX this low may be an indication of euphoria and complacency. When the VIX rises, the broad based stock indices will decline (especially the S&P500, which the VIX is directly associated with).

- A disintegration of the Eurozone (EZ) and the European Union (EU). Last year the UK voted to “BrExit,” or leave the EU and the EZ, although it wasn’t a full member (and I have doubts that the UK will ever actually leave). Catalonia (in the North East of Spain) has voted to leave Spain. Greece wants to leave the EU and the EZ. Germany has even said it wants out of the EU and EZ. This is a disaster just waiting to happen.

- There may be a looming banking crisis in Italy (and elsewhere in Europe), where many banks are becoming more and more insolvent because they’ve made too many non-performing loans (see this article). Estimates of troubled loans in Italy top the equivalent of $400 billion dollars (20% of all their loans). One of the world’s oldest and finest banks just might go bankrupt, Monte dei Paschi (see this article). An Italian banking crisis will be much more significant and devastating than any crisis in Portugal or Greece, as its economy is much larger.

In the meantime enjoy the U.S. stock indices while they are at all time highs (see Miley Cyrus on YouTube “Party in the USA”).

Currently, I like financials (see XLF, KBE, KRE, KBWR, and PSCF), as many believe that higher interest rates will benefit the financials (how rising rates benefit anyone or anything though is really anyone’s best guess- but this is a very widely held belief among investors). Also, with the 2017 resurgence of the healthcare sector (see tickers XLV, IBB, XBI, and XPH) I am starting to like XPH again, as it is lagging XLV and IBB YTD.

Long term though I really like the S&PMidCap400 (matched by ticker IJH); because mid caps tend to grow their EPS and Revenue at a faster pace and at a more consistent rate over time than (e.g. S&P500 see ticker SPY) large caps (and also when compared to (Russell2000 see ticker IWM) small caps). Higher and more consistent EPS and Revenue growth (of mid caps versus large and small caps) shows up in stock price performance. See the relative outperformance of ticker IJH (the S&PMidCap400) versus e.g. SPY (the S&P500) and IWM (the Russell2000) over nearly every three, five, and ten (or greater) year period. The S&PMidCap400 also is great to me because it avoids the hyped up large cap tech sector, laden with over valued stocks such as Netflix (which currently has a PE multiple of 220.62, according to Yahoo Finance), and Amazon (which currently has a PE multiple of 244.49 according to Yahoo Finance), and of Tesla (which has no earnings, and losses more and more with every electric car sale made).

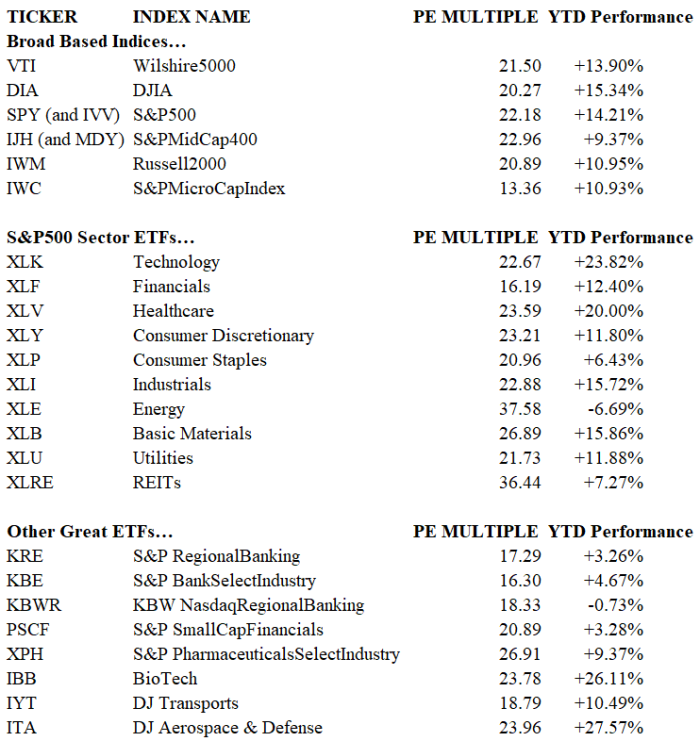

Summing things up, I wanted to give you the current PE Multiples and YTD data on many widely followed ETFs.

Lastly, checkout these links & resources to determine how the economy and markets of the USA (and of the world) are doing: The Federal Reserve’s Statement, Implementation Note, and Projection Materials (click here if you’d like to watch their last press conference); Kiplinger’s Economic Forecasts; The Economic Indicators (August 2017); JPM-AM “Guide To The Markets”; Atlanta Fed GDP Now; FRED TED Spread Data & Charting (lower figures are better); and CNN’s Fear & Greed Index.

Happy Trading!,

Andrew G. Bernhardt

PS- Be sure to checkout my Great Useful Links Page; Great News Sources; and Click here to see which Economic and Business related news articles caught my eye daily which I post on Google+.

PPS- As always, this blog is free of charge, and is for educational and for informational purposes, and is not securities advice (see my disclaimer for further details).