FOCUSING ON RISKS

Tuesday, January 10, 2017

(Just after noon eastern time)

Here are my sentiments on the securities markets as of late. Lets focus on risks.

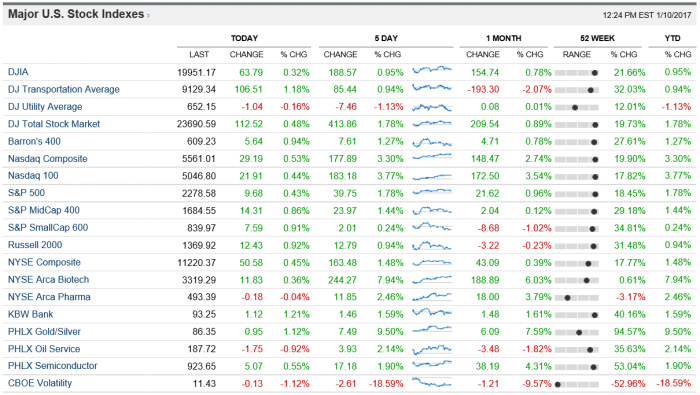

- There has been TOTALLY EXCESSIVE EUPHORIA in the stock markets since November 4, 2016. Some financials are up by +30%, +40, +50% or more since November 4th!!! This could easily result in a reality check, a pull back or correction in financials (and/or in the broad based stock indices). When financials come down, this could easily put pressure on the broad based stock indices (as financials are a huge sector allocation of the broad based indices). Monitor the euphoria of the financial ETF tickers XLF, KBE, KRE, REM, OLD, and ICF.

- The VIX is very very low right now (at 11.43 on 1-10-17 at 11:24amCT, and 32.09 is the 52 week high for the VIX). If and when the VIX rises, the stock markets will decline.

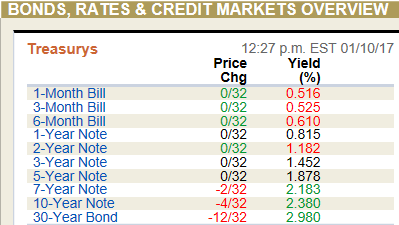

- Interest rates are too low, and when they increase, fixed income prices will decline. If rates increase enough, it will entice people out of the stock market, and into fixed income (perhaps on leverage).

- There are very high expectations for the Trump Administration, for the markets, regulatory reform, healthcare reform, and for infrastructure building. What if there are disappointments or delays?

- Trump’s nationalism and protectionism is not good for the economy, neither are taxes, tariffs, import quotas, and walls between the USA and Mexico. Hope to God we don’t have any of this nonsense.

- What if there is major “bureaucratic resistance” between the Congress and Trump? Meaning, what if the Congress blockades anything and everything that the Trump Administration wants to do?

- In other words, what if Trump can not get ACA Reforms (aka “Obamacare” or healthcare reforms through the Congress)? In other words, what if “nothing” happens?

- What if Trump can’t get Sar-Box reformed? [This would be bad for financials]

- What if Trump can’t get Dood-Frank or the Durbin Amendment reformed? [This would be bad for financials… many say that Sar-Box, Dood-Frank, and the Durbin Amendment turned our nation’s financials into “zombie banks.”]

- What if Trump “wages war” on NAFTA? [This would be bad for everyone and everything, as free trade benefits everyone!]

- What if Trump can’t get meaningful tax reforms through? [This would be bad for everyone and everything]

- What if Trump can’t get foreign earnings of major U.S. corporations repatriated to the USA? [The Congress hasn’t moved on this concept for over a decade already, and what would make them act now? The Congress is full of lazy buffoon fools who enjoy doing the wrong thing.]

- What if the European Banking Crisis gets worse? Financials in Italy are going bankrupt, due to way too many non-performing loans. What if this gets way worse?

- What if the Euro Zone and the European Union dissolves a lot faster than anyone could imagine? With e.g. the UK already voting to leave the EU on approximately June 23, 2016, what if more countries in the EU and EZ decide to leave? And what if they decide to leave sooner rather than later? E.g. what if Italy, Greece, Spain, and Portugal decide to leave?! This would mean that the EU dissolves a lot faster than many have expected, and could cause a widespread panic and/or correction in the stock markets worldwide.

- A continuation of King Dollar. This one perplexes me, but many economists believe (including Larry Summers) that a strengthening U.S. Dollar will wreak havoc on the emerging markets worldwide, leading them into a currency crisis and debt crisis of their own. This does not bode well for the stock markets worldwide. Sometimes, however I believe that a strengthening U.S. dollar will benefit the emerging markets, because they will then be selling U.S. customers (and U.S. corporations) more of their goods & services. Look e.g. what happened to the UK after its currency declined to nearly 30 to 40 year lows. Exports in the UK got stimulated and it actually led to their stock market increasing strongly. Additionally, many investors worldwide invest in U.S. Dollar denominated securities, so if their home currency declines relative to the U.S. Dollar, then they are better off as well! Lastly, a strong dollar should help to keep international commodities low such as light sweet crude oil. A strengthening U.S. dollar should help to keep inflation rates lower for longer as well.

- The USA is getting close to having $20 Trillion Dollars of debt! That’s $20,000,000,000,000.00. The USA had $19.9528 trillion of debt on January 6, 2017. Click here for an update, at the Treasury website. And remember this figure excludes Agency, and State, County, Municipal, Metropolitan, City and Local debts, Corporate, and private sector debts. We’re buried under a mountain of debt! At what point will people and investors start to say and think that deficits and debt actually matters?

For all these reasons, the stock market could easily have a pull back or a correction. Buyer beware!

Despite all those risks, I still like stocks (in the USA) for the long run. Here are some of my best hand-picked stocks for 2017 and beyond [click here], however, I think this list of stocks needs more components added in from ETF tickers REM, OLD, and KBE (click these blue links to review the components of REM, OLD, and KBE). I also feel as though 2017 will be the year of the rebound in the healthcare sector (see tickers XLV, IHE, IHI, IHF, XPH, and the more risky IBB, SBIO, GNRX, and CNCR).

In fixed income checkout tickers: PCY (30 Day SEC Yield 5.43%, Average Maturity 14.47 years); EMB (30 Day SEC Yield 5.15%, Average Maturity 10.70 years); IBDQ (30 Day SEC Yield 3.63%, Average Maturity 8.28 years); and SHYG (30 Day SEC Yield 5.34%, Average Maturity 2.33 years).

Lastly, don’t get too bullish, excited, or hyped up about DJIA 20,000. The first time the DJIA reached 10,000 was in March 29th of the year 1999! That means that since March 29, 1999 the DJIA has achieved a return of +3.964% annualized over that 17 years and 10 months! The 20 year Treasury Bond yield on March 15, 1999 was 5.79% (to keep pace with the 20 year treasury Note at 5.79% since then, over the past 17 years and ten months, the DJIA would have to immediately increase to 27,290). Investors would have been better off in fixed income since then! Hopefully, the next nearly 18 years will be better than the past 18 years.

The annualized performance since March 29, of 1999 of the Nasdaq Composite is +4.60%; The Nasdaq100 annualizes to +4.91% annualized since March of 1999. The S&P500 has returned +3.145% annualized since March 29th of 1999; the S&PMidcap400’s return since March 29th of 1999 is +8.86% annualized. The Russell2000 has returned an annualized +7.144% since March 29, 1999. I believe the best stock market index to invest in is the S&PMidCap400, matched by ticker MDY (and its cheaper generic IJH).

Happy Trading!,

Andrew G. Bernhardt

[Click here for my Great Investing Links Page]

[Click here for my Great Investing News Links Page]

[Click here for my Google+ Page, where I feature news articles that caught my eye]