Monday, October 5, 2015 – 4:45amCT

On Carl Icahn’s “Danger Ahead” Video

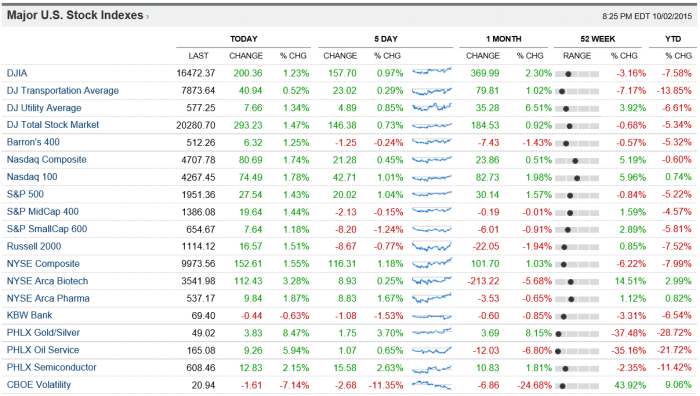

ABOVE- All Indices Performance through 10-2-15 (at the close)

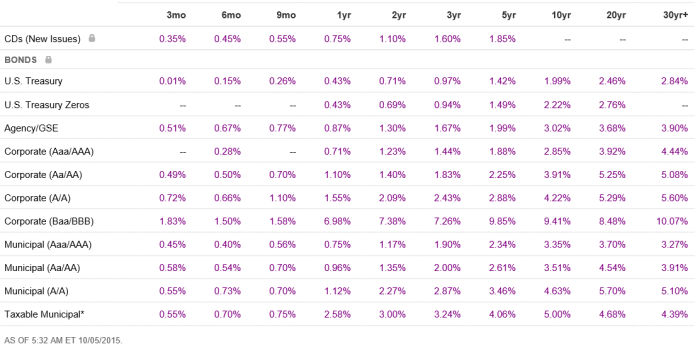

ABOVE- All Fixed Income Current Yields 10-2-15 (at the close)

Last week, on September 28, 2015, Carl Ichan (Press Here for the Wiki Article on him, if you have no idea who he is) released a video which many have brushed off as fear mongering. In his fourteen minute video, at his blog (which can be found here- Be Sure to Watch the 9-28-15 Video, “Danger Ahead”), he warns of asset bubbles, which he claims he’s “seen before” saying “he’s been around a long time,” he’s seen it “in 1969, ’74, ’79, ’87, 2000, and 2008;” Icahn worries “a time is coming that might make some of those times look pretty good.” Today, he claims he’s very very worried about the prices associated with (1) artwork, (2) stocks globally and domestic in the USA, and (3) in the high yield (“junk”) fixed income sector. Icahn also claims he supports Donald Trump, that he’s against carried interest taxation of hedge fund managers, he calls it a “tax loophole” (I guess he doesn’t want anyone in the future to be as successful as him, he wants future hedge fund managers taxed the hell out of, relative to today’s rates- I guess I’m against that, I hate higher tax rates). He’s against ZIRP (zero interest rate policy of the Federal Reserve) and believes rates should increase (and that they never should have been so low, or this low for this long). He claims ZIRP creates bubbles in assets. He claims he’s against “inversions” (where corporations take their businesses outside the USA for cheaper production of goods and services), and he wants to change the tax rates associated with “repatriation” (which everyone reasonable is all for!) U.S. Companies earnings abroad should be brought back home, to fuel growth and employment (which amounts to over $2 trillion dollars, which will not currently be brought home due to a 35% tax rate on repatriation of foreign earned income). He also claims he wants further tax reform and further immigration reform. He is also very skeptical of today’s S&P500 earnings, because he says there’s “financial engineering” gone wild, to paraphrase it. He believes that share buy backs (which reduce the number of shares outstanding, leading to artificial earnings per share increases) and mergers & acquisitions (fueled by cheap borrowing of corporations) are really clouding up the real earnings of corporations, like steroids do with athlete performance; He says he’d rather have corporations borrow cheaply to finance new property, plant, and equipment business investment, and he says there’s been little investment by corporations for decades to upgrade property, plant, and equipment, which he believes leads to less productivity. Icahn is also very concerned with ETFs and his belief that they have poor liquidity in very very volatile markets (the problem with that claim is that in very very volatile markets, NOTHING has any liquidity!). He thinks that there’s a cliff that the High Yield fixed income market is heading for in a Zero Interest Rate Party Bus… This analogy of a cliff I think is overused. The cliff, I believe, may be with the U.S. Treasury and how it borrows trillions and trillions annually for our incompetent Congress (and incompetent entire government itself) who writes huge disgusting and totally irresponsible deficits annually; They borrow as though there’s no tomorrow, many have referred to that as “the fiscal cliff.” They are crowding out investment, and crowding out borrowing, and inciting a credit crunch, just like in 2006-09, etc. If they even tried to balance the budget it would provide stimulus to the economy.

I think his “Danger Ahead” video was done on good faith, meaning he believes what he’s saying, however, I do not think there’s a huge bubble in artwork, domestic and international stocks, and also especially in the high yield fixed income sector. If there are bubbles in artwork, so be it; In stocks, everyone knows this and emerging market and foreign stocks are like lotto tickets, they’ve appreciated rapidly over the past 5 to 6 years; and high yield bonds even have sell offs occasionally, as do AAA Rated Treasury Securities (just look at tickers ZROZ and TLT, these Treasury Securities Indices have fallen off a cliff, despite recent strength!). There is no 100% “bullet proof” investment, there can be negative sentiment, negative market psychology, and bubbles over time, nearly everywhere. If there are bubbles or a looming sell off in high yield “junk” bonds, I’d say it will be contained, not as bad as 2008, and likely to present itself in corporate junk, not so much in sovereign high yield aka junk; However, local currency denominated emerging market debt (either sovereign or corporate) may have more downside to go, because I believe “King Dollar” is back, and rising interest rates will strengthen the U.S. Dollar further, which will negatively impact exchange rates globally, and emerging market currencies could depreciate rapidly versus the U.S. Dollar in the future. Emerging market currencies are dangerous and risky, so their government or corporate bonds, despite the 7.50% yields, are also dangerous and risky (See tickers CEMB, EMCB, EMCD, LEMB, PCY, and EMB). Also, click here for Payden & Rygel’s EMBI Weekly Report.

My final comments would be, why raise rates when inflation is very very low, and EPS are beginning to decline, and if global growth and U.S. growth is slowing down? There has been an earnings decline for the S&P500 this quarter, and it’s projected to get worse, before it gets better. Furthermore, why raise rates while the labor markets are weakening, due to large corporations making more and more layoffs seemingly daily? There is no reason for the Fed to raise rates, but at the same time, it’s scary they won’t be able to reduce rates (since they’re already at zero) if and when the next recession comes; If this hypothetical recession comes soon, like in the next 6 to 12 months. What will the Fed do? More quantitative easing? More bond purchases? Hopefully, they won’t experiment with negative rates, as the European central banks have experimented with. Perhaps, they’ll reduce the reserve requirement ratio, in an effort to stimulate bank lending? What will the lawyers and lawmakers do? Will they continue to believe their newest ideas and new regulations strengthen the economy and financial markets, and childishly that maybe they can outlaw recessions, or any aspect of weakness in the business cycle? They need to grow up, their stupid new regulations such as Dodd-Frank, and many others, are ridiculous! I guess we shall see how they all react in the future! It will surely be a good one!

Surprisingly, Carl Icahn’s own company Icahn Enterprises (ticker IEP, which has negative EPS) is a component of many high yield “junk” bond indices, such as ETF Ticker HYG, where fixed income issued by Icahn Enterprises amounts to approximately 0.69% of that fixed income index (see this link for the weightings and all holdings of HYG). IEP’s fixed income amounts to a weighting of 1.23% of all components of SHYG as well (click here). In another high yield fixed income ETF, ticker JNK, Icahn Enterprises amounts to a 0.65% allocation of that index. In ticker SJNK IEP’s bonds amount to 1.15% of the index (click here). Know that Icahn’s Icahn Enterprises fixed income has declined substantially this year, as has his company stock; No wonder he’s so bearish, and says he’s been very very hedged.

Here are some recent articles related to all this:

- http://www.thestreet.com/story/13308038/1/carl-icahn-is-wrong-there-s-no-debt-crisis-looming.html

- http://www.wallstreetdaily.com/2015/09/02/fed-interest-rates-recession/

- http://www.cnbc.com/id/103022365

- http://www.barrons.com/articles/BL-231B-9474 “Time To Buy Emerging Market Gov. Bonds”

- http://www.cnbc.com/id/103048392 (I believe the stock markets won’t rise if there’s a EPS recession)

- http://www.reuters.com/article/2015/09/30/imf-lagarde-idUSL1N1201A320150930

- http://www.reuters.com/article/2015/10/01/us-markets-stocks-idUSKCN0RU1BI20151001

- http://www.cnbc.com/2015/10/04/emerging-market-turmoil-flashes-warning-lights-for-global-economy.html

- http://www.wsj.com/articles/lawrence-summers-still-disagrees-with-janet-yellen-1443728960

- http://www.cnbc.com/id/103047442

- http://www.wsj.com/articles/the-power-of-the-purse-1443569801

- http://theaustrianview.com/2015/09/29/the-bond-bubble-cant-last-forever-the-junk-bonds-will-be-hit-first/

- http://davidstockmanscontracorner.com/this-bear-is-just-waking-from-hibernation/

- http://davidstockmanscontracorner.com/weve-seen-this-picture-before-global-markets-down-13-trillion-already/

- http://davidstockmanscontracorner.com/bofa-issues-dramatic-junk-bond-meltdown-warning-this-train-wreck-is-accelerating/

- https://www.bogleheads.org/wiki/Emerging_market_bonds

- http://www.investopedia.com/articles/investing/072915/doddfrank-creates-liquidity-crunch-bonds.asp

- http://webreprints.djreprints.com/3645380735365.html

- http://www.bloomberg.com/news/articles/2015-09-29/carl-icahn-s-scary-movie-michael-p-regan

- http://blogs.wsj.com/moneybeat/2015/09/29/carl-icahn-is-skeptical-of-the-ma-boom/

- http://blogs.wsj.com/economics/2015/09/29/imf-flashes-warning-lights-for-18-trillion-in-emerging-market-corporate-debt/

- http://www.cnbc.com/id/103033999 (“Goldman Sachs Cuts Forecast for S&P500”)

- http://www.cnbc.com/2015/09/25/maybe-we-need-a-government-shutdown-commentary.html (By Larry Kudlow)

- http://www.cnbc.com/2015/09/22/pimco-could-be-impossible-for-fed-to-raise-rates.html

- http://www.cnbc.com/2015/09/21/bogle-the-fed-did-the-right-thing.html

~ Andrew G. Bernhardt

[See My “Great Useful Links” Page] [See My “Great News Sources” Page]