May 25, 2015

Stock & Fixed Income Market Checkup

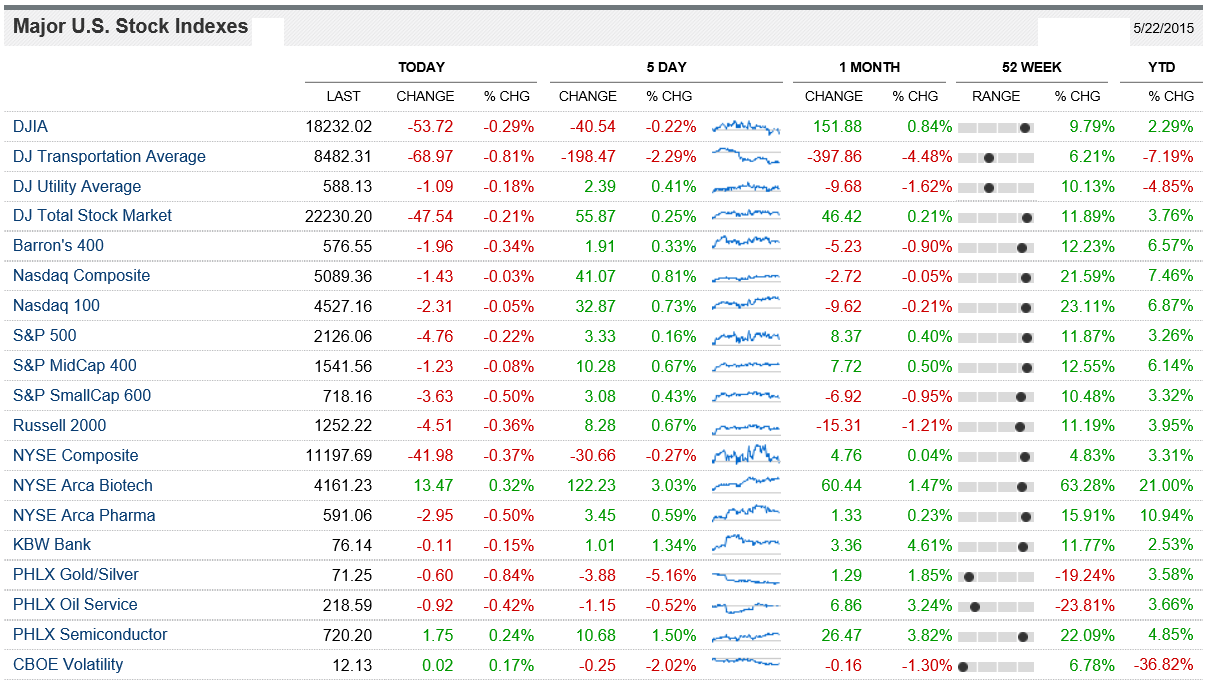

As you can see the markets have done fairly well YTD. The S&PMidCap400 has returned +6.14% YTD, the S&P500 has returned +3.26% YTD, the DJIA has returned +2.29% YTD, Russell 2000 has retuned +3.95% YTD, and the Nasdaq 100 has returned +6.87% YTD. Biotech is up roughly +21% YTD. Know also that YTD the VIX has declined about -36.82%. For a great assessment of the U.S. Economy (and the worldwide economy) press here, for the latest edition of The Economic Indicators, the April 2015 edition.

Some are voicing concern over the Dow Jones Transportation index, which is -7.19% YTD, however, if you go back more than YTD, say 1, 2, 3, or 5 years on a chart of the Transports against the DJIA, the Transports are outperforming; So to me there’s not much to be concerned about regarding that divergence YTD of Transports vs. the DJIA.

I’m currently rooting for the DJIA, matched by the ETF ticker DIA, as it has the lowest PE Multiple of all the Major U.S. Stock indices, and also the highest dividend yield relative to all other major U.S. Stock indices (with the exception of Utilities). The DJIA has also lagged the other major market indices YTD, and I think it will eventually catch up. I’d wait for a pullback before getting too aggressive with the indices here. I think the DJIA will close around 20,000 near year end, as Jeremy Siegel has speculated publically, even if we get a mini correction soon, or a full blown ten percent (or more) correction.

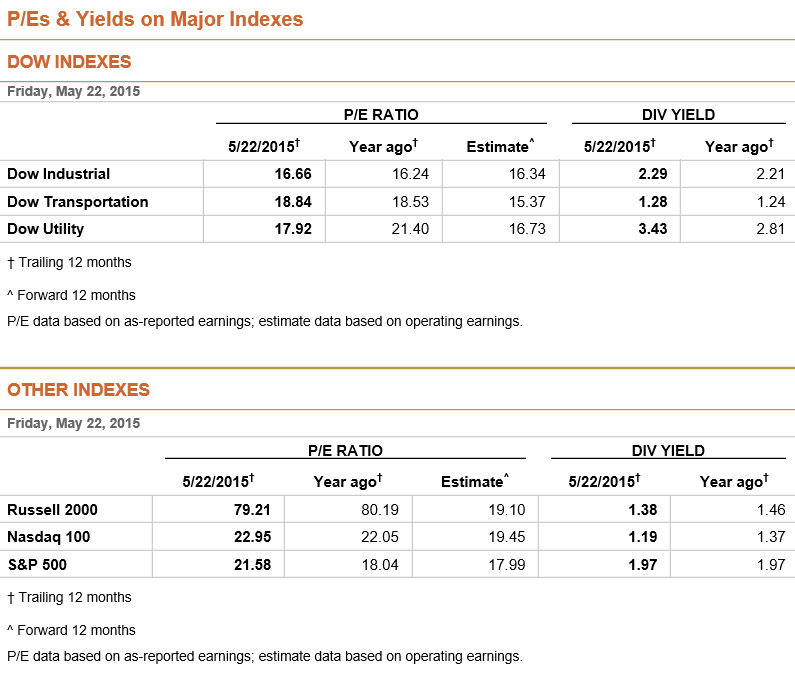

I’ve annualized the DJIA since about March of 1999 to the present, about 16.25 years ago (when it was at 10,000) it annualizes to +3.77%. This is well below the historical norms of roughly +7.50%. What has hindered the equity markets over the past 15 years or so has been the Roaring 90s, which set us up for the Tech Bubble of the year 2000 (the Nasdaq peaked at 5,132 on March 10, 2000- It still hasn’t reached break even with that figure from over fifteen years ago!), and what I describe as “The Greater Depression” of late 2007 to roughly early 2009. The S&P500’s performance over the past 16.25 years has been weaker than the DJIA due to its technology exposure (tech has been the biggest disappointment over the past 16.25 years… “Tech” is a four letter word!). The best equity performance over the long run can be found in the S&PMidCap400, which has had significantly more consistent and stronger earnings growth, and better annualized returns versus all other major U.S. market indices (see ETF ticker MDY).

In my view currently the VIX has gotten very very low, and should be indicating that you should be cautious going forward. Low VIX indicates euphoria and mania in the equity securities markets. There’s only been a handful of days where the VIX has been so low, for very long, and when it spikes, or increases, the equity markets can come tumbling down fast. This brings opportunity.

There’s an inverse correlation noteworthy of significance between the trajectory of the VIX, and the trajectory of every major stock market that there is, so when the VIX declines, the markets rise; and when the VIX ascends, the markets fall. I think since it’s so very low right now, it will likely increase, and the markets will decline.

My crystal ball tells me that we’re in for a mini-correction, of 3 to 5 percent before the markets will begin their ascent to new highs again. I’d remain cautious (holding cash) until we get a pull back in stock prices.

The main concerns going forward, are a low VIX; markets are at nearly all time highs; Greece is totally insolvent and may exit the Euro currency and the EU; and economic data has been weak in the USA and elsewhere; If and when Greece exits, investors will worry about Italy, Spain, and Portugal exiting the Euro currency and EU itself. Additionally, China is slowing (despite its recent booming stock market), Europe isn’t really that strong (and the European stock and fixed income markets may be in bubble territory, as is the case for the Euro currency itself); Russia is really hurting due to low oil prices; and Africa is fundamentally totally speculation (and is classified as a “frontier market;” There may be HUGE opportunities there in the future over the long run), and Central and South America are in a slump (Brazil has been very weak for many years now). Japan has also been weak, despite its stock market ascending. This tells me the backdrop for the economy worldwide is not really improving that greatly. PE Multiples are neither low, nor high, but they’re definitely closer to high, than low. Fear and market psychology over Greece’s insolvency could push the equity markets lower worldwide over the coming days and weeks.

Here (above) are the up and coming Greek Debt Payments… Many are expecting ultimately a default, which could bring about market turmoil.

Above is the Greek IMF required payments; Many are expecting a default, which would not bode well for the equities markets, or the fixed income markets worldwide. There definitely could be some turmoil over Greece’s conduct and behavior going forward.

As you can see (above) the PE Multiples are on the rise over the past 12 months, and dividend yields are mixed but on aggregate are flat to up for 12 months. Press here for the S&PMidCap400’s PE Multiple, at the SSGA’s ETF MDY website, which posts the fund’s characteristics and the index’s characteristics [Click here for the same info on the ETF ticker DIA, the ETF matching the performance of the Dow Jones Industrial Average] [Click here for fund info and index info on SPY and the S&P500] [Click here for fund and index info on QQQ and the Nasdaq-100] [Click here for Fund and Index Info on the ETF IWM and the Russell 2000] [Click here for fund and index info on ETF VTI, formerly known as the Wilshire 5000, now called the Dow Jones U.S. Total Stock Market Index].

I’d wait for a pullback (holding big cash positions) before getting fully invested and/or leveraged in equities, and more aggressive with the equities markets. I think bonds are in for more dire straights, and interest rates are going to rise in my opinion going forward; Rates were at totally unprecedented lows recently. How rates ever got that low, and stayed that low for so long, is beyond me! I can’t believe anyone would lend money to the U.S. Treasury at e.g. 2.33% for 30 year bonds a few weeks ago!!! Those rates were obscene, and were totally irrational! Fixed income investors will be treading water for quite some time in my view. Those invested at the long end are in for some more trouble I think. I believe that Treasury Security investors will be SHOCKED as to how much they can lose in e.g. 30 year Treasuries, as the duration and interest rate risk is very high (see tickers TLT and ZROZ, both of which are well off their 52 week highs!). Surprisingly, junk bonds and the high yield markets are nicely priced right now, I’m expecting more of a selloff to continue in Government bonds worldwide than junk and high yield bonds. You can see evidence of this in tickers: ZROZ, TLT, TIP, EMB, PCY, HYG, JNK, QLTC, etc.

Know historically the stock markets are weak in the months of February, May, and September, according to Barron’s Magazine (I would dispute and research February allegedly being historically weak, but I’ll just report what Barron’s has said recently).

I believe there will be fear mongers warning of a recession looming, due to the weak retail sales, weak producer price index, weak industrial production, an weak consumer sentiment; Not to mention the turmoil in Greece. I still think that after we get a mini correction the economy, in the USA and worldwide, will improve, bringing equity prices up (after a potential mini correction or full blown summer correction). There may have been a weak spot in the economic data due to a rather harsh winter season and very bitterly cold temperatures, which held back and discouraged the consumer (the biggest part of the economy) during the first quarter.

I believe there is increased risk of the first rate hike by the FOMC rate hike in 2016 by Yellen, not in September or December of 2015. Of course, there will be journalists saying and wondering if she’ll raise rates in June 2015. I believe she’s nearly spelled it out, repeatedly, that the FOMC will not raise rates in June, and at the earliest they might raise rates in September. Once we get closer to 2016, gurus will say and wonder if she’ll raise rates during an election year. I believe interest rates, at the short end, are going to remain low for quite some time (while rates at the long end will increase).

There are many who say higher rates will harm REITs (see the ETF ICF), and that it should benefit financials such as those found in the ETF XLF, and regional financials such as those found in the ETF tickers KRE and KBE.

I believe eventually the paranoia over higher rates will subside. The end of the world is not coming due to higher interest rates at the short end, or even at the long end. I do not believe the U.S. will have another recession until about late 2017 or 2018 (at the earliest), and for that reason I think the equity markets will continue to grind higher (after we get through some short term volatility and turmoil). I’m expecting a slight pullback and mini correction, followed by rebounds and a slow grind to higher stock prices for the next year or two.

Just because the market has risen sharply since March of 2009, does not mean it can not continue to increase. After all the annualized performance of the major U.S. Stock Indices since 1999 or 2000 (of roughly zero to roughly plus three-point-seven-seven) has not been anywhere near the longer term historical averages, of approximately plus seven and a half percent per year.

Happy trading!

Andrew G. Bernhardt