Tuesday, March 31, 2015

“End of the Quarter Update”

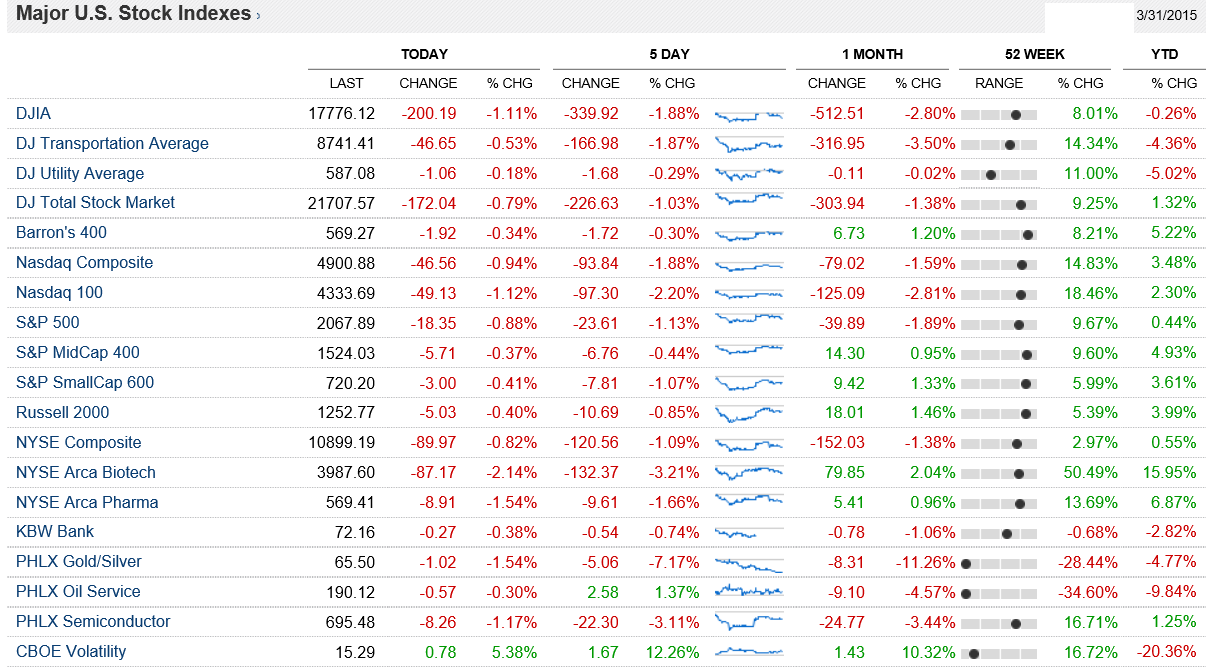

Here’s how the equity indices finished for the day, week, month, past 52 weeks, and for the quarter (see YTD) figures.

Stock Market Performance through 3-31-15

Current risks I believe include a continuation of Russia’s sabre rattling, default risk of Greece, foolish negative interest rates in europe leading to a rapidly weakening euro currency and a strengthening U.S. dollar. A strong dollar and weaker euro will lead to a wider current account deficit in the U.S., to less exports, more imports, and diminished profits from abroad from the multinational corporations. Further risks include, a weak recovery (actually the weakest economic recovery after any recession on record in the USA) from the “greater recession” of late 2007 through 2009, a fragile and weak labor market recovery, weak job recovery, high rates of unemployment, an weak housing market recovery, an enormous U.S. federal government debt outstanding growing annually from enormous deficits, and foreign instability abroad as well as major geopolitical risks. All this threatens strong growth ahead. In the distant future there are also major demographic headwinds looming in the USA and abroad (due to, I believe, birth control pills), which may cause major federal budget deficits in the coming decades since women have been having fewer children, and they’ve been having fewer children later in life; This strains generous entitlement programs, such as Medicare, Medicaid, and Social Security. This coming demographic problem may be reason to keep interest rates quite low for some time, well into the future. Additionally, with weak readings of the CPI-U Janet Yellen is likely to keep the Federal Funds rate low for the foreseeable future; I believe that rates may not rise until at least September, if not until 2016. There are also worries that profits may actually decline for this quarter, or depending on who you’re listening to, that they could disappear all together. Also, don’t forget that China and Japan are already beginning to slow down.

Looking on the bright side, rates can’t really seem to move lower, in my view either at home, or especially abroad (Negative rates in Europe! Seriously!?). Rates in Europe for example are already negative one hundred and seventy five basis points, and when rates rise abroad in the future, in europe, that won’t bode well for their equity or bond markets (I believe it will be party over, aka game over for europe when rates launch off of negative rates). This makes the USA look on a relative basis more attractive. Additionally, the weak soft patch of economic data in the USA may have been due to the late blizzard like conditions in the north east, which was very unseasonal. If and once demand picks up again in the north east, economic data could come in nicely on the positive surprise side. Stronger data could coincide with and warrant higher stock prices going forward. I believe this will materialize.

Happy trading!

Andrew G. Bernhardt