Weekend Update

And On The Securities Action of Friday, January 30, 2015

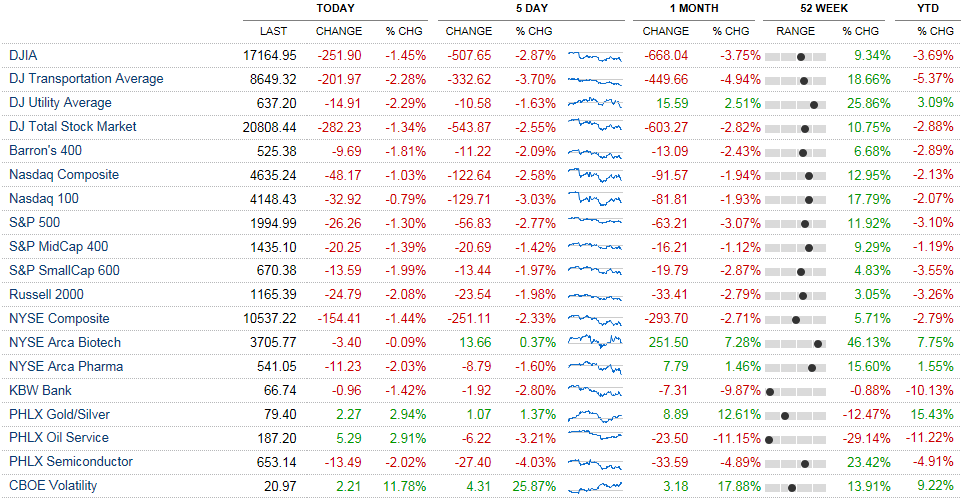

BIG SELLOFF ON WALL STREET! Friday was a tough day for equities at Nassau & Wall, Stocks slumped mostly in the final 30 minutes of action. The VIX surged +11.78% or +2.21 points to close at 20.97. The S&P500 was down for most of the trading day, but reached an intra-day bottom around 11am central time, before reversing and rallying back to unchanged; it then actually registered a slight advance into positive territory for a short time, before reversing again, and selling off hard in the final 30 minutes. Sovereign fixed income rallied, while high yield corporate fixed income sold off. On Friday the DJIA fell -251 points or -1.45% to 17,164.95. The S&P500 was down -26.26 points or -1.30% to 1,994.99. The S&PMidCap400 fell -20.25 points or -1.39% to close at 1,435.10. For the week most major U.S. Stock indices shed two to three percentage points, except the S&PMidCap400 which traded down -1.42% for the week. Despite Friday’s action, I’m still bullish and believe stock prices will go higher.

The DJIA is now -5.18% off its highest point reached in the past 12 months, the S&P500 is -4.71% of its 12 month peak, the S&PMidCap400 is -2.92% off its 12 month peak, the Nasdaq Composite is -3.73% off its 12 month peak, and the Russell 2000 is now -4.59% of its 12 month peak, the Wilshire 5000 is now -4.29% off its peak. XLF, an etf basket of financials, was -1.62% to 23.01, and now stands 8.47% off its peak reached in the past 12 months. Despite today’s bearishness, the highly telegraphed in advance global slowdown, and Russia’s turmoil, I remain optimistic, and I don’t see any real reason to panic.

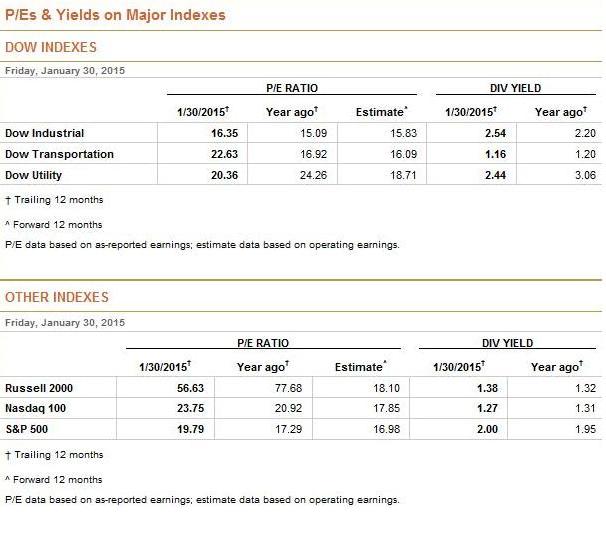

It’s hard to be bearish on the DJIA when the PE Multiple is so low at 16.35 when compared to the other indices, additionally its dividend yield has increased in the past 12 months and is substantially higher than the other indices.

USO (oil) traded sharply higher +6.83% to close at 17.82, XLE was up +0.87% to 75.55, RSX was down -1.28% to 14.62, CUBA was +2.75%% to 8.96. I believe that oil will trade sharply higher and lower, but I believe it may have reached rock bottom on January 29th. [http://finance.yahoo.com/futures]

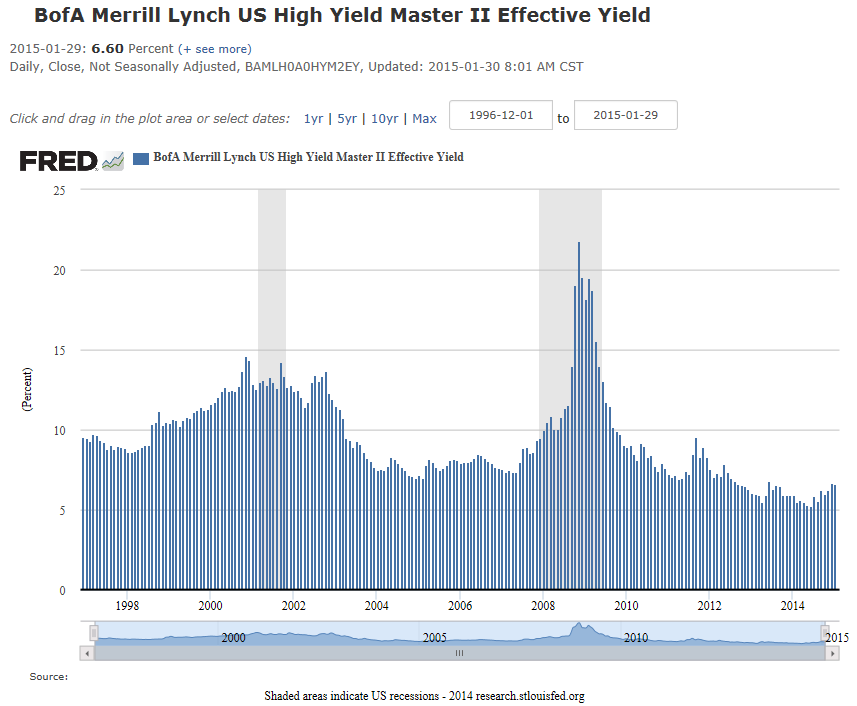

In the Fixed income markets, ZROZ traded higher, up +2.89% to 138.99, TLT traded up +1.77% to 138.28, IEF traded higher by +0.88% to 110.55, TIP was up +0.72% to 115.63. EMB was up +0.09% to 111.76, PCY was up +0.14% to 28.78, HYG was down -.28% to 90.23, JNK was down -0.21% to 38.94, and QLTC traded down by -0.88% to 48.57. The 30 year Treasury yield settled at 2.25%, the 10 year Treasury yield settled at 1.68% [data from here: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield]. I continue to believe, and will reiterate, that if oil can ever find rock bottom, and/or stabilize in a trading range, or start to appreciate, that there will be some major opportunities in the energy sector in equities, and in their high yield fixed income; Also I believe that when oil stabilizes (or begins to appreciate) that there will be some major opportunities in high yield fixed income funds, such as the ones listed above, EMB, PCY, HYG, JNK, and QLTC. Lastly, with the current yield on the DJIA at 2.54%, and the 30 year Treasury bond yield at 2.25%, it’s difficult to be bearish on equities. Everyone knows rates are going to eventually go higher; But what is everyone going to do next, sell bonds and purchase stocks?! Imagine that when it develops when rates begin to rise. Perhaps they’ll (investors will) “sell everything”? Below I have obtained some historical noteworthy data from the Federal Reserve Economic Data research center website, which plots the effective yield of high yield fixed income.

The US Dollar traded slightly lower versus the Euro on Friday, the Euro gained approximately +0.20%, to 1.1285. I continue to believe the Ruble and the Euro are still too high, and will further deteriorate, making the dollar stronger. Check up on current cross rates here: http://finance.yahoo.com/currency-investing/majors. Russia roiled the markets by reducing its key interest rate from 17% to 15%; This sparked a Ruble sell off, the U.S. Dollar can now purchase 69.65 Rubles. QE is nearly everywhere now, which may bode well for equities globally this year.

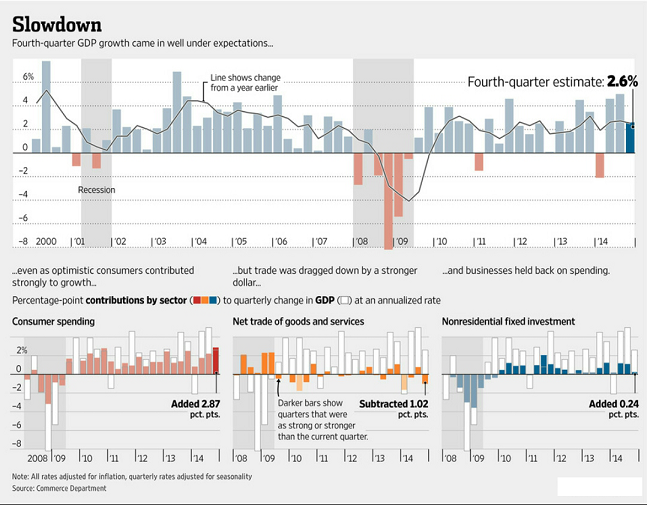

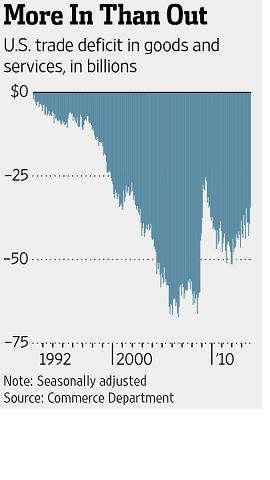

I believe the catalysts for today’s stock market selloff were the economic data releases, Russia’s spur of the moment rate reduction, and worried on Greece’s debt and its ability to pay interest on its sovereigns fixed income. U.S. Economic data releases were all quite good, except GDP, which came in weaker than was expected, at +2.6% for the quarter, when economists were widely expecting 3.2%. For highlights on the GDP report (1 page) click here: [http://www.bea.gov/newsreleases/national/gdp/2015/pdf/gdp4q14_adv_fax.pdf]; For the full 17 page report click here: [http://www.bea.gov/newsreleases/national/gdp/2015/pdf/gdp4q14_adv.pdf]. Economists speculate that the trade deficit, which widened, due to a strong dollar, creating an environment of fewer exports, and more imports, scraped a full percentage point off of this quarter’s advance GDP figure. The chain deflator (a measure of inflation/deflation) came in at 0.00, consensus was for +1.0%, and the Employment Cost Index came in at +0.6% while economists were expecting an increase of +0.3% to +0.5%. The Chicago PMI came in at 59.4 while expectations were for 57.5 to 58.0. Lastly, Michigan Consumer Sentiment came in at 98.1, expectations were for 97.5 to 98.2. Below I’ve obtained a nice trade deficit chart. I’d expect with a strengthening dollar the trade deficit will increase.

Next week, I believe economic data releases will likely be dominated by the labor force figures due on the 6th. Economists are expecting unemployment to hold steady at 5.6%. I believe there’s risk that figure could come in better than expected. Also next week newsworthy reports will be Monday’s Personal Income and Outlays, PMI Manufacturing index, ISM Manufacturing Index, and Construction spending. Tuesday, Motor Vehicle Sales and Factory Orders are due for release. Wednesday, the ADP Employment Report is due, as is ISM Non- Manufacturing Index, and the EIA Petroleum Status Report. Thursday, International Trade, and Jobless Claims, as well as Productivity and Costs are due.

In notable eps reports due next week, I think CMG will be amusing, as will WYNN, both eps are reports due after the market close on Tuesday the 3rd. On the 4th after the close YUM and GMCR both report their eps, GMCR expectations are always quite high; It’s hype. Thursday the 5th will see CME and TWTR eps both after the close, TWTR will surely be surrounded by hype, if I had to guess. Surely, these reports will be entertaining.

I remain bullish still on equities, for 2015; I do fear that we could have another day or two of selling before we get liftoff again though. I continue to believe (as I’ve said earlier) that the stronger dollar and weakening oil prices will bode well for consumer sentiment and for consumer spending, which is the largest component of GDP. I think also a strengthening U.S. dollar, weaker inflation (aka disflation), and a weakening global economic outlook will result in the Federal Reserve raising rates at the earliest this summer, if not delaying further, possibly until early 2016.

In other news, there were stunning eps reports at MA and V; while CVX beat expectations but saw its eps decline by -38%. MSFT is now down roughly -19.28% off it’s peak reached in the past 12 months, it was down by another -3.83% on Friday alone. Also MCD was down on Friday by -0.89% and is now -10.93% off its peak reached at some point in the last year. The new MCD president said that they’re bringing back their old “I’m Lovin’ it!” slogan. The new CEO of MCD also said that for a limited time, 1% of customers in select restaurants will get their food for free, if they publically display an act of love; e.g. a child hugging their parents. Before you know it the Federal Trade Commission in a joint effort with the Department of Justice will be investigating MCD for price discrimination and/or fraud! CVX traded lower by -0.46%, and is now -24% off its peak reached in the past 12 months. The entire energy sector has been slaughtered, as CNBC’s Jim Cramer would say. GOOGL missed its 7.11 eps target, but rallied strongly Friday(!!), trading up by +24.32 or +4.74% to 537.55 per share, I had speculated that it might move roughly 22 dollars higher or lower in an earlier blog post; and I suggested that perhaps (for educational purposes) a bull call ratio back spread with net credit characteristics may be lucrative (when and if also combined with a bear put ratio back spread with net credit characteristics). Happy earnings speculation! GOOGL now stands -12.60% off its peak of the past 52 weeks. Lastly, AMZN handily beat its eps forecasts, and traded higher by +44.75 per share or +13.71% to 354.53.

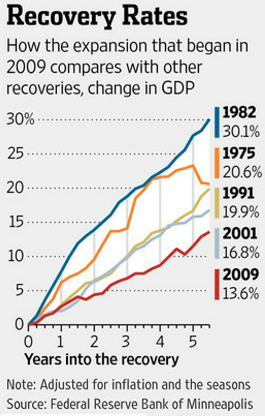

Yesterday Bill Gross wrote on what he described as the anemic recovery in the USA, see the chart below. I brought up the point that yes, it may be a weak GDP rebound recovery, compared to previous recoveries. While the GDP recovery and growth rates have not been so strong, relative to the past’s recovery rates, the stock market performance has been very strong since early March of 2009; A lot stronger than prior recoveries! We won’t likely see +200% (or greater) returns in equities over any six year period again, anytime soon in the United States. 200% in six years annualizes to +20.09%!!! Yes that’s right, +20.09% for six years in a row on average! Derived from 3^(1/6). Still I don’t believe that equities are overvalued, they’re reasonable on a PE multiple basis. The alternative of U.S. Treasuries (and other high credit quality sovereigns) at exceptionally low yields (or even negative yields elsewhere in sovereigns worldwide) is the conundrum we find ourselves in today.

It’s time for the 2015 Super Bowl, XLIX of the New England Patriots vs. the Seattle Seahawks. Stay tuned for the commercials! They’re priced this year at 30 seconds for $4,500,000; which is $150k per second. Thirty second ads were priced at $3.8 million in 2013, and $4 million in 2014. That’s a lot of money for those intangible airwaves!

The markets are making me a little jittery here, it’s been a tough week or two for equities. My crystal ball tells me, if Greece can get its act together, and if Russia will stop saber rattling, then the markets would have nowhere to go but higher. Eventually, with oil at such depressed prices, Russia will not be able to afford its military fiascoes against its neighbors, so the end of Russia’s foolishness is near. In the meantime the political and financial market instability (the geopolitical risk) in that region of the world will be stomach churning. The VIX in my view doesn’t have much higher to go, if at all higher, I couldn’t or don’t really see it breaking 25, or especially 30. If it gets through 30, all bets are off, and I’d expect a 10% correction (or worse) would have occurred, or would surely be in the cards. Still if that’s in our future, I’d expect some major buying opportunities. Longer term, I’m bullish. I think the USA is not going to have a recession for at least another year or two, if not further away into the distant future. Full steam ahead.

By Andrew G. Bernhardt